Retiring with ₹6 crore in your bank account—enough to live your dream life, travel the world, or simply relax without financial worries. Now, picture achieving this by setting aside just ₹50,000 every month through a Systematic Investment Plan (SIP). Sounds ambitious? It’s not only possible but also within reach if you harness the power of long-term investing and compounding. we’ll dive into how a ₹50,000 monthly SIP can transform into a ₹6 crore corpus in 20 years, reveal the best mutual funds to consider in 2025, and share actionable tips to make your retirement dreams a reality

Table of Contents

What Is a SIP and Why Should You Care?

A Systematic Investment Plan (SIP) is a simple yet powerful way to invest in mutual funds. Instead of dropping a lump sum, you invest a fixed amount—say, ₹50,000—every month. This money goes into a mutual fund of your choice, where it’s managed by experts to grow over time. SIPs are wildly popular in India because they’re affordable, disciplined, and tap into the magic of compounding—where your returns generate more returns.

Why care? Because SIPs make wealth-building accessible. You don’t need a fortune to start; you just need consistency. Over 20 years, a modest monthly SIP can snowball into a life-changing sum, like ₹6 crore. Ready to see how? Let’s crunch the numbers.

The Math Behind ₹50K Monthly SIP Turning Into ₹6 Crore

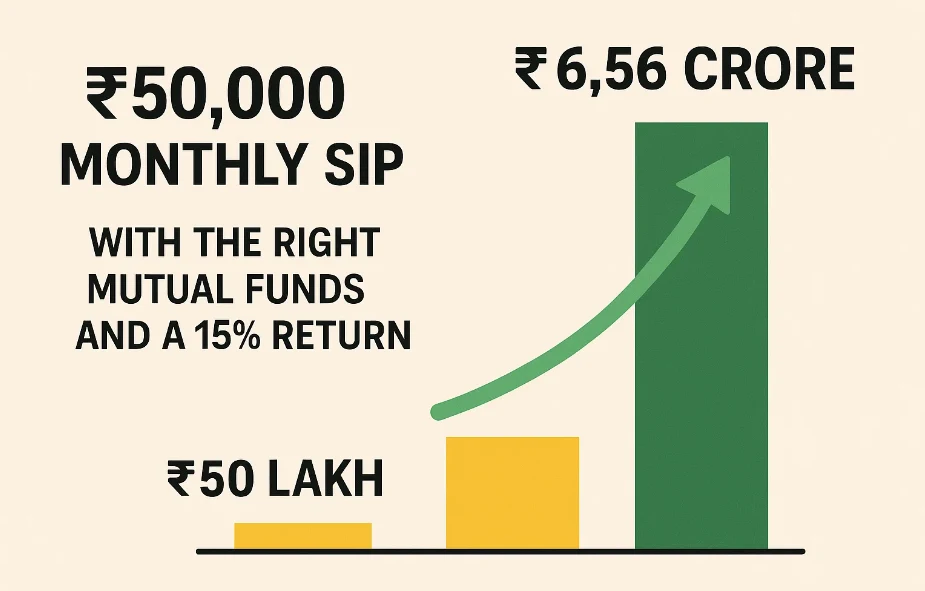

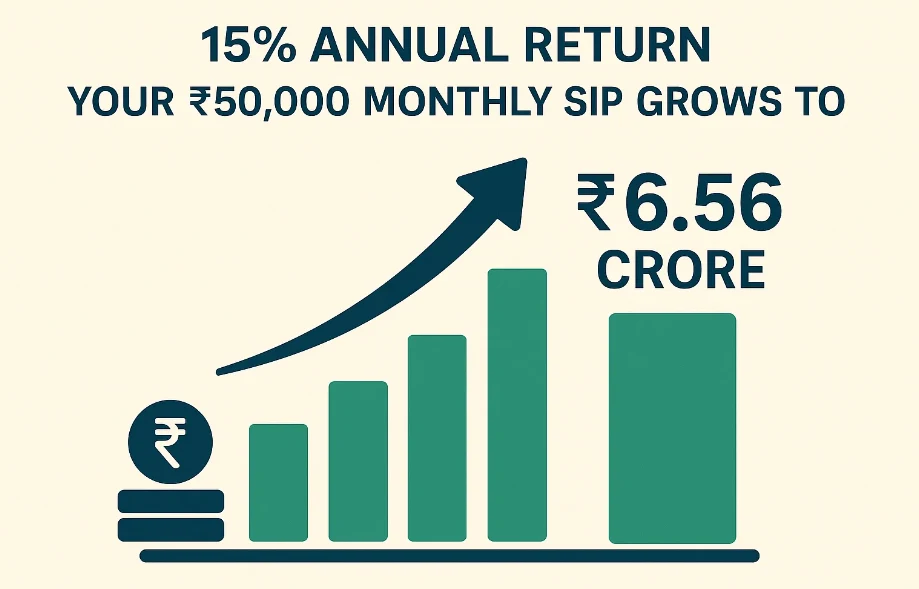

Let’s get to the exciting part: how does ₹50,000 a month become ₹6 crore in 20 years? It’s all about the rate of return and time. Equity mutual funds in India have historically delivered 12-15% annual returns over the long term. For this example, we’ll assume a 15% annual return—a realistic target with the right funds.

Here’s the breakdown:

- Monthly Investment (SIP Amount): ₹50,000

- Total Time: 20 years = 240 months

- Annual Return: 15%

- Monthly Return: Approximately 1.1714% (calculated as ( (1 + 0.15)^{1/12} – 1 ))

The formula for the future value of a SIP is:

FV = P × [((1 + r)^n – 1) / r]

Where:

- FV = Future Value

- P = Monthly SIP amount (₹50,000)

- r = Monthly return (0.011714)

- n = Number of months (240)

Plugging in the numbers:

- (1 + 0.011714)^240 ≈ 16.366

- [(1.011714)^240 – 1] ≈ 15.366

- 15.366 / 0.011714 ≈ 1,311.6

- 50,000 × 1,311.6 ≈ ₹6,55,80,000 (₹6.56 crore)

So, with a 15% annual return, your ₹50,000 monthly SIP grows to ₹6.56 crore in 20 years. Even at a more conservative 12% return, you’d still end up with around ₹4.69 crore—not too shabby!

Here’s a quick table to visualize the growth:

| Years | Total Invested (₹) | Value at 12% (₹) | Value at 15% (₹) |

|---|---|---|---|

| 5 | 30,00,000 | 41,14,000 | 44,89,000 |

| 10 | 60,00,000 | 1,13,00,000 | 1,32,00,000 |

| 15 | 90,00,000 | 2,39,00,000 | 3,06,00,000 |

| 20 | 1,20,00,000 | 4,69,00,000 | 6,56,00,000 |

Key Takeaway: Your total investment of ₹1.2 crore balloons to ₹6.56 crore at 15%—that’s over 5 times your input, thanks to compounding!

Why Compounding Is Your Secret Weapon

Albert Einstein reportedly called compounding the “eighth wonder of the world,” and for good reason. When you invest via SIPs, your money doesn’t just grow linearly—it multiplies exponentially. Every month, your returns get reinvested, earning returns on themselves. Over 20 years, this snowball effect turns small, regular investments into a massive corpus.

Here’s a simple analogy: think of your SIP as planting a tree. The first few years, it’s just a sapling (small gains). But give it time, and it becomes a towering giant (₹6 crore). The earlier you plant, the bigger it grows.

Quote: “Compounding is like planting a seed today that grows into a forest tomorrow. Patience is the water it needs.” – Warren Buffett (adapted)

How to Choose the Best Mutual Funds for Your SIP

Not all mutual funds are created equal. To hit that ₹6 crore target, you need funds that consistently deliver high returns. Here’s what to look for:

- Past Performance: Check 5-10 year returns. Funds with a strong track record are safer bets.

- Fund Manager Expertise: A skilled manager can navigate market ups and downs.

- Expense Ratio: Lower fees (e.g., below 1%) mean more money stays invested.

- Risk Profile: Match the fund to your comfort level—equity funds for growth, hybrid for stability.

- Diversification: Funds investing across sectors reduce risk.

Pro Tip: Look for funds with a CAGR (Compound Annual Growth Rate) of 12-15% over the long term.

Top Mutual Funds for SIP in 2025

Based on current trends and historical performance, here are five stellar mutual funds to consider for your ₹50,000 monthly SIP in 2025. (Note: Always consult a financial advisor before investing.)

- SBI Bluechip Fund

- Category: Large-Cap

- Avg. Return: ~13-14% (past 10 years)

- Why Choose: Stable returns with top companies like HDFC Bank and Reliance.

- HDFC Mid-Cap Opportunities Fund

- Category: Mid-Cap

- Avg. Return: ~15-16%

- Why Choose: High growth potential for risk-takers.

- Mirae Asset Emerging Bluechip Fund

- Category: Large & Mid-Cap

- Avg. Return: ~16-17%

- Why Choose: Balanced growth with a stellar track record.

- Axis Long Term Equity Fund

- Category: ELSS (Tax-Saving)

- Avg. Return: ~14-15%

- Why Choose: Tax benefits under Section 80C + solid returns.

- ICICI Prudential Equity & Debt Fund

- Category: Hybrid

- Avg. Return: ~12-13%

- Why Choose: Lower risk with equity-debt mix.

Bullet Points: Why These Funds Shine

- Proven consistency over 5+ years

- Managed by top-tier fund houses

- Aligned with long-term wealth goals

- Suitable for different risk appetites

The Power of Starting Early and Staying Disciplined

Time is your biggest ally in the SIP game. Starting at 25 vs. 35 can make a massive difference. Here’s why:

- Early Start: More months for compounding to work its magic.

- Discipline: Regular investments, even during market dips, average out your costs (called rupee cost averaging).

For example, if you skip the first 5 years and start at ₹50,000/month for 15 years at 15%, you’d get ~₹3.06 crore—half of what 20 years yields!

Quote: “The best time to plant a tree was 20 years ago. The second-best time is now.” – Chinese Proverb

Tip: Set up an auto-debit SIP to stay consistent—no excuses!

Step-Up SIPs: Turbocharge Your Corpus

Want to hit ₹6 crore faster? Consider a Step-Up SIP, where your monthly amount increases annually (e.g., by 10%). Starting at ₹50,000, you’d invest ₹55,000 in year 2, ₹60,500 in year 3, and so on. At 15% returns, this could push your corpus past ₹8 crore in 20 years!

Here’s a snapshot:

- Year 1 SIP: ₹50,000/month

- Year 10 SIP: ~₹1,29,000/month

- Total Invested: ~₹2.38 crore

- Final Value: ~₹8-9 crore (at 15%)

Table: Step-Up SIP Growth (10% Annual Increase, 15% Return)

| Years | Monthly SIP (₹) | Total Invested (₹) | Corpus (₹) |

|---|---|---|---|

| 5 | 80,525 | 48,31,500 | 66,00,000 |

| 10 | 1,29,687 | 1,13,00,000 | 1,95,00,000 |

| 20 | 3,36,585 | 2,38,00,000 | 8,50,00,000 |

Addressing Risks and Concerns

SIPs aren’t risk-free—markets can be volatile. But here’s the good news:

- Rupee Cost Averaging: Buying more units when prices dip balances your costs.

- Long-Term Horizon: Over 20 years, short-term dips smooth out.

- Diversification: Good funds spread risk across stocks and sectors.

Still worried? Start with a hybrid fund or consult an advisor to match your risk tolerance.

FAQs: Your SIP Questions Answered

Q1: Can I start a SIP with less than ₹50,000?

Yes! Many funds allow SIPs from ₹500/month. Start small, then scale up.

Q2: What if I miss a SIP payment?

No penalty—your existing investments keep growing. Just don’t make it a habit!

Q3: Are SIPs tax-free?

Returns from equity funds held over 1 year face 10% LTCG tax (above ₹1 lakh). ELSS funds offer Section 80C deductions.

Q4: How do I pick the best fund?

Research past returns, fees, and risk. Use tools like Moneycontrol or consult an advisor.

Q5: Can I stop my SIP anytime?

Yes, SIPs are flexible—pause or stop without penalties.

Conclusion: Your Path to ₹6 Crore Starts Now

Retiring rich isn’t a fantasy—it’s a plan. A ₹50,000 monthly SIP, with the right mutual funds and a 15% return, can grow to ₹6.56 crore in 20 years. Add a step-up strategy, and you could aim even higher. The secret? Start early, stay disciplined, and pick winners like SBI Bluechip or Mirae Asset Emerging Bluechip.

So, why wait? Open a mutual fund account today, set up your SIP, and watch your wealth grow. Your future self will thank you.