1. Introduction

For Indian investors in 2026, building a ₹1 Crore portfolio is more achievable than ever before.

India’s economy is projected to grow around 7.5% in FY26, making it one of the fastest-growing major economies in the world. At the same time, the Nifty 50 index is targeting the 30,000 mark by late 2026, creating strong wealth-creation opportunities for retail investors.

Millions of Indians are entering the stock market through mutual fund SIPs and digital investment platforms. This shift has created a powerful environment for long-term investors who follow disciplined strategies.

This guide explains how beginners can build a ₹1 Crore portfolio step by step, using current market data from 2026 and growth forecasts up to 2032.

If you start early, stay consistent, and invest wisely, reaching ₹1 Crore in the next decade is not just possible—it is highly realistic.

2. Market Overview

The investment landscape in 2026 is supported by strong domestic demand, rising digital adoption, and increasing participation from retail investors.

Monthly mutual fund SIP inflows have crossed ₹25,000 crore, showing that Indian households are increasingly choosing equity markets for long-term wealth creation.

India is also moving toward upper-middle-income status, with per capita income reaching approximately ₹2.49 lakh in 2026.

Lower borrowing costs are supporting economic expansion. The RBI repo rate stands near 5.25%, encouraging credit growth across sectors such as housing, infrastructure, and consumer spending.

Meanwhile, technological innovations such as AI-powered investment tools and digital portfolio management have improved market analysis and forecasting accuracy by nearly 15% in 2026.

Table 1: India Economic Projections (2026–2030)

| Indicator | 2026 Projection | 2030 Forecast | Growth Type |

|---|---|---|---|

| Real GDP Growth | 7.5% – 7.6% | 6.5% – 7.0% | Resilient |

| Per Capita Income | ₹2.49 Lakh | ₹3.32 Lakh | Accelerated |

| Inflation (CPI) | 3.2% – 4.5% | 4% Stable | Controlled |

| Nifty 50 Target | 30,000 | 50,000 | Structural Bull |

| Rural Consumption | 8.4% YoY | 10.5% CAGR | Rising |

These trends highlight why 2026–2032 could become one of India’s strongest wealth-building periods.

3. Key Data Insights

Compounding remains the most powerful wealth-creation tool for long-term investors.

In 2026, many millennial investors are adopting step-up SIP strategies, where investment amounts increase every year.

A simple 10% annual increase in SIP contributions can reduce the time required to reach ₹1 Crore by nearly 5–7 years.

Market data also shows strong sector performance:

- Small-cap funds currently deliver 25.48% 3-year rolling returns as of March 2026.

- Large-cap indices are expected to generate 12–14% CAGR over the next decade.

- Emerging sectors such as Renewable Energy and Artificial Intelligence are projected to grow 18–25% annually.

Table 2: Power of Step-Up SIPs (Target ₹1 Crore)

| Monthly SIP | Annual Step-Up | Duration | Expected CAGR | Final Value |

|---|---|---|---|---|

| ₹15,000 | 0% | 18 Years | 13% | ₹1.10 Cr |

| ₹15,000 | 10% | 13 Years | 13% | ₹1.04 Cr |

| ₹25,000 | 5% | 12 Years | 13% | ₹1.02 Cr |

| ₹10,000 | 15% | 14 Years | 13% | ₹1.12 Cr |

This data clearly shows how increasing investments gradually can significantly accelerate wealth creation.

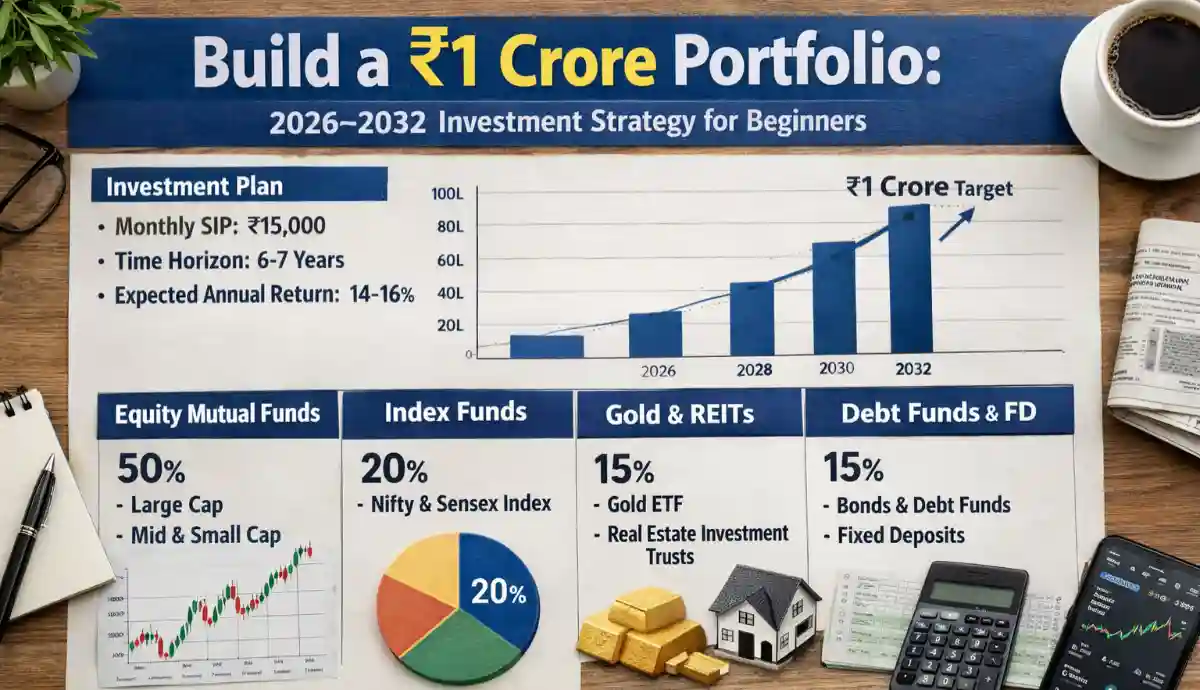

4. Investment Strategy

For beginners starting in 2026, diversification is essential.

A balanced allocation strategy helps reduce risk while maintaining strong growth potential.

Financial planners recommend the 70:20:10 rule:

- 70% Equity

- 20% Debt

- 10% Gold or Alternatives

Equity investments should include flexi-cap funds, which dynamically adjust allocations across large, mid, and small companies.

Choosing direct mutual fund plans can reduce expenses by 1%–1.5% annually, improving long-term returns significantly.

Additionally, modern investment platforms now allow AI-based tax-loss harvesting, potentially improving after-tax returns by around 1.5% per year.

Regular portfolio rebalancing—ideally every six months—helps maintain proper asset allocation.

Table 3: Optimized Portfolio Allocation for Beginners

| Asset Class | Allocation | Investment Vehicle | Expected ROI |

|---|---|---|---|

| Large Cap Equity | 40% | Nifty 50 Index Fund | 12.5% |

| Mid & Small Cap | 30% | Active Mutual Funds | 18% |

| Debt Funds | 20% | Corporate Bond Funds | 7% |

| Gold/Silver | 10% | Sovereign Gold Bonds | 9% |

This strategy balances growth, stability, and protection against economic shocks.

5. Growth Forecast (2027–2032)

The next decade will likely be driven by structural sectors transforming India’s economy.

One of the biggest opportunities lies in Renewable Energy and Green Hydrogen. India plans to reach 500GW renewable capacity by 2030, creating massive investment potential.

The Electric Vehicle ecosystem is also expanding rapidly with battery manufacturing and charging infrastructure.

Manufacturing is expected to grow significantly due to Production Linked Incentive (PLI 2.0) schemes, potentially increasing manufacturing’s share of GDP to 25% by 2030.

Technology spending is shifting toward Generative AI, automation, and cybersecurity, with expected 20% annual growth rates.

Meanwhile, rising incomes will drive higher demand for healthcare, insurance, and premium housing.

Table 4: Sector Growth Forecast (2027–2032)

| Sector | Growth Catalyst | Expected CAGR | Investment Grade |

|---|---|---|---|

| Renewable Energy | 500GW Target | 22% | High |

| Information Technology | AI & Cloud | 18% | Medium-High |

| Financial Services | Digital Lending | 15% | Core |

| Infrastructure | Logistics & Housing | 12% | Stable |

| Healthcare | Rising Income Levels | 16% | Defensive |

Investors who focus on these sectors could benefit from India’s long-term economic transformation.

6. Risk Analysis

Every investment strategy involves risk, especially during periods of rapid economic expansion.

Global geopolitical tensions remain a key concern. If crude oil prices rise above $70 per barrel, India’s GDP growth could slow by around 25 basis points.

Small-cap stocks are currently trading at premium valuations, meaning investors should maintain a long-term horizon of at least 7 years.

Inflation is another important factor. If inflation rises above 5%, the RBI may tighten monetary policy, which could temporarily impact market growth.

Before beginning the journey to ₹1 Crore, investors should build an emergency fund covering at least six months of expenses.

Table 5: Risk vs Reward Matrix

| Investment Type | Volatility | 5-Year Return Est. | Risk Strategy |

|---|---|---|---|

| Nifty Index Fund | Low | 75–85% | Long-term holding |

| Small Cap Funds | High | 150–180% | Systematic investing |

| Hybrid Funds | Medium | 60–70% | Rebalancing |

| Thematic Funds | Very High | 200%+ | Limit exposure |

Understanding risk ensures stable and sustainable wealth creation.

7. Conclusion

Building a ₹1 Crore portfolio is not about perfect market timing—it is about discipline, patience, and consistency.

Starting a ₹15,000 monthly SIP with a 10% annual increase could help investors achieve this milestone in approximately 13 years.

Focus on high-growth sectors like renewable energy, fintech, and digital infrastructure, while keeping large-cap funds as the portfolio foundation.

The investment environment in 2026 is one of the most promising decades for Indian investors.

Those who begin early, invest regularly, and maintain diversification are most likely to achieve financial independence.

Table 6: ₹1 Crore Investment Checklist

| Step | Action | Timeline |

|---|---|---|

| 1 | Complete e-KYC & open demat account | Immediate |

| 2 | Start ₹15K monthly SIP | Within 7 days |

| 3 | Increase SIP by 10% | Every year |

| 4 | Review portfolio | Every 6 months |

| 5 | Add alternative assets | After ₹10L corpus |

FAQs

1. Can beginners really build a ₹1 Crore portfolio?

Yes. If equity markets deliver 13–15% CAGR, a ₹15,000 monthly SIP with annual step-up can reach ₹1 Crore in roughly 13 years.

2. Which mutual funds are best for growth?

Flexi-cap and mid-cap funds currently offer strong growth potential while maintaining diversification.

3. How does inflation impact the ₹1 Crore goal?

Inflation reduces purchasing power. A ₹1 Crore corpus today may equal ₹60–70 lakh in real value by 2040, so investors should aim for ₹1.5–2 Crore long-term.

4. Should gold be part of the portfolio?

Yes. Keeping 5–10% allocation in gold can hedge against currency depreciation and global economic uncertainty.

5. What happens if the market crashes?

Corrections are normal. Historically, 15–20% corrections are often followed by strong recoveries within 12 months.

Pro Tip:

Starting today matters more than waiting for the perfect moment.

Even a small SIP today could become the foundation of your ₹1 Crore portfolio tomorrow.