You’re sitting on ₹5 lakh—maybe it’s your hard-earned savings, a bonus, or an inheritance. It’s not pocket change, but it’s not enough to retire on either. Now, imagine turning that ₹5 lakh into ₹1 crore. Not overnight, not through some get-rich-quick scheme, but through a smart, steady plan that works. Sounds like a dream, right? It’s not—it’s real, and it’s doable.

Table of Contents

I’m not here to throw jargon at you or sell you a fairy tale. I’m here to map out a journey—a successful investment map—that can take you from ₹5 lakh to ₹1 crore over time. Whether you’re a newbie who’s never invested a rupee or someone who’s dabbled in stocks and SIPs, this guide is for you. We’ll unpack the basics, explore your options, and build a plan that fits your life. Expect real talk, relatable examples, and actionable steps. Ready to grow your wealth? Let’s get started.

Why Investing Matters: The Power of Starting Now

Before we dive into the how, let’s talk about the why. Why should you care about turning ₹5 lakh into ₹1 crore? Because money that sits idle is money that’s losing value. Inflation chips away at it every year—think of it as a slow leak in your savings bucket. Investing plugs that leak and turns your bucket into a fountain.

The secret sauce here is compounding. It’s not magic; it’s math. When you invest, your money earns returns, and those returns earn more returns. The longer you let it roll, the bigger it grows. Let’s break it down with a quick example:

- You invest ₹5 lakh at a 10% annual return.

- After 10 years, it’s ₹12,96,871.

- After 20 years? ₹33,63,749.

- Give it 25 years, and you’re at ₹54,17,019—over halfway to ₹1 crore!

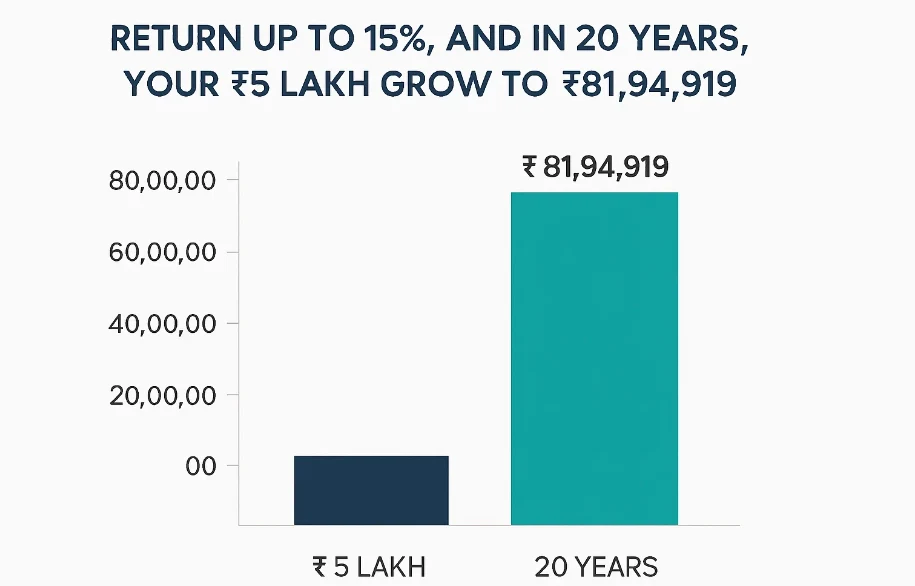

Now, crank that return up to 15%, and in 20 years, your ₹5 lakh balloons to ₹81,94,919. That’s close to your crore, and we haven’t even added more money yet. The takeaway? Time is your biggest ally. Start now, and you’re already ahead.

Setting Your Sights on ₹1 Crore

So, you’ve got ₹5 lakh, and you want ₹1 crore. Awesome. But how do you make that happen? First, let’s set the stage with a clear goal. Ask yourself:

- How much time do I have? Are you 25, dreaming of early retirement, or 40, planning for your kids’ future?

- How much risk can I stomach? Are you cool with ups and downs, or do you need steady wins?

- What’s my starting point? Is ₹5 lakh all I’ve got, or can I add more over time?

For this guide, let’s assume you’re aiming for ₹1 crore in 20 years—a realistic timeline for most. To get there from ₹5 lakh, you’ll need an average annual return of about 15%. Is that doable? Yes, with the right mix of investments. Let’s explore your options next.

Your Investment Toolkit: Where to Put Your Money

Turning ₹5 lakh into ₹1 crore means picking the right tools for the job. You wouldn’t build a house with just a hammer, right? Same deal here—you need a mix of investments to balance growth, safety, and flexibility. Here’s your toolkit:

1. Stocks: The Growth Engine

Stocks are shares in companies. When those companies do well, your money grows—sometimes a lot. The Indian stock market has delivered average returns of 12-15% over the long term, but it’s a rollercoaster.

- Pros: High growth potential, easy to buy/sell.

- Cons: Risky, needs research or a pro’s help.

Tip: New to stocks? Start with a demat account and dip your toes in with blue-chip companies or equity mutual funds.

2. Mutual Funds: The Smart Shortcut

Mutual funds pool your money with others to buy a diversified basket of stocks or bonds. They’re managed by experts, so you don’t have to sweat the details. SIPs (Systematic Investment Plans) let you invest small amounts monthly—perfect if you want discipline.

- Pros: Diversified, beginner-friendly, flexible.

- Cons: Fees, market risk.

Fun Fact: Over 10 years, many equity mutual funds in India have delivered 12-18% returns. That’s crore territory!

3. Real Estate: The Tangible Option

Real estate is tricky with ₹5 lakh—you’re not buying a flat in Mumbai with that. But options like REITs (Real Estate Investment Trusts) or fractional ownership platforms let you invest in property without breaking the bank.

- Pros: Steady income, inflation protection.

- Cons: Less liquid, market-dependent.

4. Fixed Income: The Safety Net

Think fixed deposits (FDs), government bonds, or corporate bonds. These give you predictable returns with low risk—great for balancing your portfolio.

- Pros: Stable, low risk.

- Cons: Lower returns (5-7%), inflation lag.

5. Alternatives: Gold and Beyond

Gold’s a classic—think of it as your financial insurance. Cryptocurrencies? They’re wild cards—huge wins possible, but so are losses.

- Pros: Gold hedges inflation; crypto has high potential.

- Cons: Gold grows slowly; crypto’s volatile.

Here’s a quick look at how ₹5 lakh could grow with different options:

| Investment | Annual Return | 10 Years | 20 Years |

|---|---|---|---|

| Fixed Deposit | 6% | ₹8,95,424 | ₹16,03,567 |

| Equity Mutual Fund | 12% | ₹15,52,974 | ₹48,23,255 |

| Stocks | 15% | ₹20,23,274 | ₹81,94,919 |

Stocks and mutual funds are your heavy hitters for reaching ₹1 crore. But don’t put all your eggs in one basket—mix it up.

Crafting Your Investment Plan

You’ve got your tools—now let’s build the plan. A solid portfolio spreads your ₹5 lakh across assets to match your risk level. Here’s a sample for a moderate risk-taker:

- 50% in Equity Mutual Funds (₹2.5 lakh): Growth driver.

- 30% in Debt Funds/FDs (₹1.5 lakh): Stability anchor.

- 10% in Gold (₹50,000): Inflation shield.

- 10% in REITs (₹50,000): Real estate kicker.

If you’re younger and bolder, bump up equity to 70%. Closer to retirement? Lean heavier on debt. The key is diversification—it’s your shield against market mood swings.

Expert Quote: “Do not save what is left after spending, but spend what is left after saving.” – Warren Buffett

Buffett’s onto something. Invest first, then live off the rest—it’s the mindset shift that builds wealth.

Supercharging with SIPs

What if ₹5 lakh isn’t your starting point? No worries—you can still hit ₹1 crore with regular investing. Enter SIPs. Let’s say you invest ₹10,000 monthly. Here’s how it grows:

| Years | 10% Return | 12% Return | 15% Return |

|---|---|---|---|

| 10 | ₹20,48,582 | ₹23,00,632 | ₹27,56,589 |

| 15 | ₹41,72,582 | ₹50,31,242 | ₹66,32,589 |

| 20 | ₹75,93,582 | ₹98,92,582 | ₹1,39,32,589 |

At 15%, ₹10,000 a month gets you past ₹1 crore in 20 years. No lump sum needed—just consistency. Small steps, big wins.

Keeping Your Portfolio on Track

Investing isn’t “set it and forget it.” Markets move, life changes—you’ve got to stay in the driver’s seat. Review your portfolio yearly. If equity jumps to 60% because of a bull run, sell some and buy more debt or gold to rebalance. It’s like pruning a plant—keeps it healthy.

Taxes: Don’t Let Them Eat Your Gains

Taxes can nibble at your returns, so let’s get smart about them:

- Equity (Stocks/Mutual Funds): Long-term gains over ₹1 lakh? 10% tax.

- Debt Funds: 20% tax with indexation on long-term gains.

- FDs: Interest taxed at your slab rate.

Pro Move: Invest in ELSS mutual funds—they’re tax-savers under Section 80C and grow your money. Double win.

Case Study: Priya’s Path to ₹1 Crore

Let’s make this real with Priya, a 30-year-old teacher with ₹5 lakh from her savings. She wants ₹1 crore by 50 for her daughter’s education and a comfy retirement. Here’s her plan:

- Starting Point: ₹5 lakh.

- Allocation: 60% equity mutual funds (₹3 lakh), 30% debt funds (₹1.5 lakh), 10% gold (₹50,000).

- Extra Boost: ₹10,000 monthly SIP in equity funds.

- Returns: 14% on equity, 7% on debt, 5% on gold.

Here’s how it plays out:

| Year | Equity (60%) | Debt (30%) | Gold (10%) | SIP Growth | Total |

|---|---|---|---|---|---|

| 5 | ₹6,00,000 | ₹2,07,000 | ₹63,800 | ₹8,50,000 | ₹17,20,800 |

| 10 | ₹12,00,000 | ₹2,95,000 | ₹80,000 | ₹23,00,000 | ₹38,75,000 |

| 15 | ₹24,00,000 | ₹4,20,000 | ₹1,00,000 | ₹50,00,000 | ₹79,20,000 |

| 20 | ₹48,00,000 | ₹6,00,000 | ₹1,30,000 | ₹1,00,00,000 | ₹1,55,30,000 |

By year 20, Priya’s past ₹1 crore—way past, actually. She hit her goal by blending a lump sum with SIPs and sticking to her plan. Could you be the next Priya?

Expert Wisdom to Guide You

Let’s lean on some pros for inspiration:

Rakesh Jhunjhunwala: “Investing is not about timing the market, but time in the market.”

Stay in the game—that’s where the magic happens.Play the long game, not the quick gamble.

These giants remind us: Patience and consistency beat flash-in-the-pan moves every time.

Conclusion: Your Crore Is Waiting

From ₹5 lakh to ₹1 crore—it’s not a pipe dream; it’s a plan. You’ve got the map now: Start with the basics, pick your investments, diversify like a pro, and keep at it. Whether it’s stocks, SIPs, or a bit of gold, every rupee you invest today is a step toward that crore tomorrow.

This isn’t about luck—it’s about you taking charge. Feel that spark? That’s your future calling. Start your SIP today, talk to an advisor, or open that demat account now. Your ₹1 crore journey begins with one bold move. What’s yours?

FAQs: Your Burning Questions Answered

1. How long does it take to grow ₹5 lakh to ₹1 crore?

With a 15% return, about 20 years. At 10%, closer to 25. Time and returns are your levers—adjust them to fit your life.

2. What’s the safest way to reach ₹1 crore?

Low-risk options like FDs (6-7%) won’t cut it alone—you’d need more time or money. Mix in some equity for growth, balanced with debt for safety.

3. Can I do this without ₹5 lakh upfront?

Absolutely! Invest ₹10,000 monthly via SIPs at 15%, and you’ll hit ₹1 crore in 20 years. Consistency trumps lump sums.

4. Which investment is best for beginners?

Mutual funds via SIPs. They’re simple, diversified, and managed by pros—your low-stress entry to wealth-building.

5. How do taxes affect my goal?

They take a bite—10% on equity gains over ₹1 lakh, 20% on debt with indexation. Plan smart with tax-saving options like ELSS.

6. What if the market crashes?

Crashes happen. Stay calm, keep investing—markets recover, and long-term players win. Think years, not days.