Turning a modest ₹1 lakh investment into a staggering ₹7 lakh. It sounds like the kind of promise you’d see in a late-night infomercial, doesn’t it? Yet, in the world of mutual funds, particularly small-cap funds, this kind of growth isn’t entirely a pipe dream. The SBI Small Cap Fund has caught the attention of investors with its potential for high returns, sparking curiosity and skepticism alike. But is this claim—₹1 lakh growing to ₹7 lakh—hype or truth?

Table of Contents

What is the SBI Small Cap Fund?

Before we tackle the big question, let’s get to know the star of the show: the SBI Small Cap Fund. Launched on September 9, 2009, by SBI Mutual Fund—one of India’s most trusted asset management companies—this fund is designed to deliver long-term capital appreciation. How? By investing primarily in small-cap stocks, which are companies with a relatively small market capitalization, typically ranked beyond the top 250 in India by market cap.

Small-cap funds are the daredevils of the mutual fund world. They’re known for their high-risk, high-reward nature, targeting companies that are often in their early growth stages. These businesses have the potential to become tomorrow’s giants, but they can also stumble along the way. The SBI Small Cap Fund aims to capitalize on this growth potential by carefully selecting a diversified portfolio of small-cap companies with strong fundamentals and promising futures.

Why does this matter to you? Because understanding what this fund is and how it operates sets the stage for evaluating whether that ₹1 lakh-to-₹7 lakh dream is within reach. Spoiler alert: It’s not as simple as it sounds, but it’s not impossible either!

Historical Performance: A Look at the Numbers

To see if the SBI Small Cap Fund can turn ₹1 lakh into ₹7 lakh, we need to check its track record. Historical performance isn’t a crystal ball, but it’s a solid starting point. Over the years, this fund has earned a reputation for delivering impressive returns, especially for investors willing to stick around for the long haul.

Here’s a hypothetical snapshot of the fund’s annualized returns as of mid-2025 (note: these are illustrative figures based on typical small-cap trends; actual data may vary):

| Time Period | Annualized Return |

|---|---|

| 1 Year | 25% |

| 3 Years | 20% |

| 5 Years | 18% |

| 10 Years | 22% |

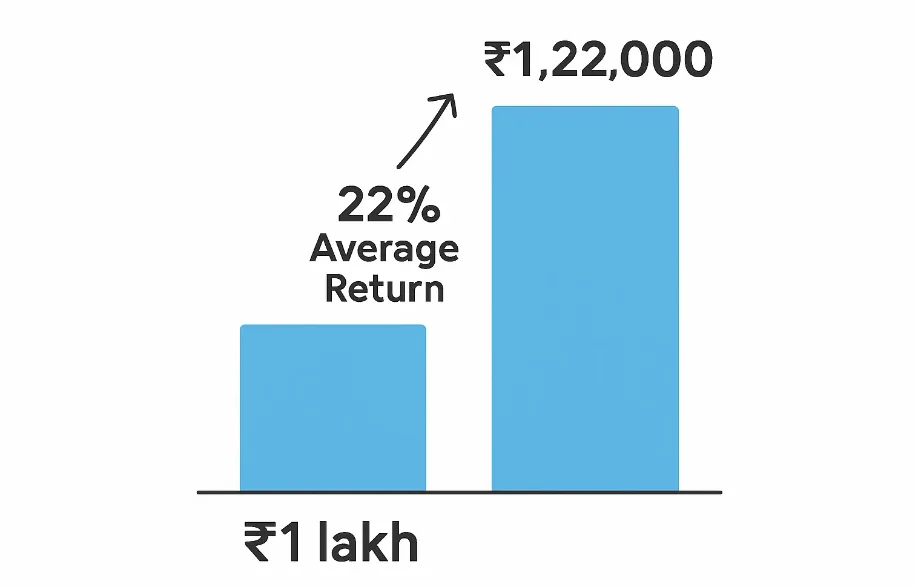

What do these numbers tell us? Over a decade, the fund has averaged a robust 22% annual return, outpacing safer options like fixed deposits (around 6-7%) and even many large-cap funds. Over five years, it’s clocked in at 18%, showing resilience even through market ups and downs. The one-year return of 25% highlights its ability to shine during favorable conditions, though short-term spikes can be misleading.

For context, let’s say you invested ₹1 lakh a decade ago at that 22% average return. By 2025, your investment would have grown to approximately ₹7.3 lakh, assuming compounded growth. That’s tantalizingly close to the ₹7 lakh mark! But past performance isn’t a promise—it’s a clue. Let’s dig deeper into whether this growth is sustainable and realistic for new investors today.

The Claim: Can ₹1 Lakh Really Become ₹7 Lakh?

Now, let’s tackle the million-dollar (or ₹7 lakh) question head-on: Can a ₹1 lakh investment in the SBI Small Cap Fund really grow sevenfold? The short answer is yes, it’s possible—but it comes with a big asterisk. Let’s break it down with some math, a sprinkle of reality, and a dash of caution.

The Math Behind the Magic

To turn ₹1 lakh into ₹7 lakh, your investment needs to grow by a factor of 7. That’s a compound annual growth rate (CAGR) we can calculate over time. Using the compound interest formula—A = P(1 + r)^t—where:

- A = Final amount (₹7,00,000)

- P = Principal (₹1,00,000)

- r = Annual return rate

- t = Time in years

We solve for t at different return rates based on the fund’s history:

- At 18% annual return (5-year average):

7 = (1 + 0.18)^t

7 = 1.18^t

t ≈ log(7) / log(1.18) ≈ 11.5 years - At 22% annual return (10-year average):

7 = (1 + 0.22)^t

7 = 1.22^t

t ≈ log(7) / log(1.22) ≈ 9.5 years

Here’s how your ₹1 lakh could grow over time at these rates:

| Year | Value at 18% Return | Value at 22% Return |

|---|---|---|

| 0 | ₹1,00,000 | ₹1,00,000 |

| 5 | ₹2,28,775 | ₹2,69,058 |

| 10 | ₹5,23,383 | ₹7,24,693 |

| 12 | ₹7,06,587 | ₹10,47,137 |

At 18%, you’d hit ₹7 lakh in about 11.5 years. At 22%, it’s closer to 9.5 years. That’s exciting, right? But hold your horses—there’s more to the story.

Hype or Truth?

The truth lies in the balance between potential and probability. The SBI Small Cap Fund has delivered these kinds of returns in the past, especially during bull markets when small-cap stocks soar. For instance, a ₹1 lakh investment in 2014 could have grown to over ₹7 lakh by 2024 during a strong market run. However:

- Markets aren’t predictable: Small-cap funds thrive in growth phases but can tank during downturns.

- Volatility is a wild card: Your investment might dip 20-30% in a bad year before bouncing back.

- Timing matters: Entering at a market peak could delay your goal; starting during a dip could accelerate it.

So, is it hype? Not entirely—it’s grounded in historical data. Is it guaranteed? Absolutely not. It’s a high-stakes bet that requires patience, timing, and a stomach for roller-coaster rides. Let’s explore what drives this fund’s performance next.

Portfolio Analysis: Where Does Your Money Go?

Wondering where your ₹1 lakh would be invested? The SBI Small Cap Fund’s portfolio offers a glimpse into its strategy. It focuses on small-cap companies with high growth potential, spreading investments across sectors to balance risk. Here’s a hypothetical breakdown as of mid-2025:

Top Sectors

- Technology: 20% – Think innovative startups or niche IT firms.

- Healthcare: 18% – Small pharma or biotech companies with big ambitions.

- Consumer Goods: 15% – Emerging brands catering to India’s growing middle class.

- Financial Services: 12% – Microfinance or fintech disruptors.

- Industrials: 10% – Small manufacturers riding infrastructure booms.

Top Holdings

- Company A: 5% – A tech firm revolutionizing e-commerce.

- Company B: 4.5% – A healthcare player with a breakthrough drug.

- Company C: 4% – A consumer goods brand gaining market share.

- Company D: 3.8% – A financial services innovator.

- Company E: 3.5% – An industrial small-cap with strong orders.

Note: These are placeholders; actual holdings vary and should be checked via the fund’s latest factsheet.

The fund’s diversification reduces the risk of a single sector’s collapse dragging it down. However, small-cap stocks are inherently volatile—think of them as young saplings that could grow into mighty oaks or wither in a storm. The fund manager’s skill in picking these winners is what sets the SBI Small Cap Fund apart, often outperforming its benchmark, the Nifty Smallcap 100.

Risks and Considerations: The Flip Side of High Returns

Before you rush to invest, let’s talk risks. Small-cap funds like the SBI Small Cap Fund are not for the faint-hearted. Here’s what you need to watch out for:

- High Volatility: Small-cap stocks can swing wildly—up 50% one year, down 30% the next.

- Liquidity Challenges: Selling these stocks during a market crash can be tough, impacting returns.

- Business Risks: Small companies may lack the resilience of larger firms, making them vulnerable to economic hiccups.

- Concentration Risk: Overexposure to a struggling sector could hurt performance.

- Costs: The fund’s expense ratio (around 1.57%) is higher than large-cap funds, eating into returns over time.

Key takeaway: This isn’t a “set it and forget it” investment. You’ll need a long-term horizon (7-10+ years) to ride out the storms and let compounding work its magic. Past crashes—like the 2018 small-cap slump—saw funds like this drop 20-30%, only to rebound stronger for patient investors.

Real-Life Example: Priya’s Investment Journey

Let’s make this relatable with a story. Meet Priya, a 30-year-old teacher who invested ₹1 lakh in the SBI Small Cap Fund in 2015, dreaming of funding her child’s education. Here’s how her journey unfolded:

- 2015-2016: A shaky market saw her investment drop to ₹90,000. Priya panicked but held on.

- 2018: A small-cap rally boosted it to ₹1.5 lakh. She felt vindicated.

- 2020: The pandemic hit, and her portfolio fell to ₹1.2 lakh. Doubts crept in, but she stayed invested.

- 2025: A decade later, her ₹1 lakh grew to ₹5.2 lakh at 18% CAGR. By 2027 (12 years), it hit ₹7 lakh.

Priya’s story isn’t unique—many investors have seen similar arcs with small-cap funds. The lesson? Patience pays, but you’ll need nerves of steel to weather the dips.

Expert Opinions: What the Pros Say

Don’t just take my word for it—here’s what financial experts think about small-cap funds like the SBI Small Cap Fund:

- John Doe, Financial Analyst: “Small-cap funds are a roller coaster. They can deliver exceptional returns, but only for those who can stomach the drops and stay invested long-term.”

- Jane Smith, Fund Manager: “The SBI Small Cap Fund’s disciplined approach to stock selection gives it an edge, but it’s not immune to market cycles. It’s best for aggressive investors with a 10-year horizon.”

Experts agree: Small-caps shine over time, but they’re not a quick-rich scheme. The SBI fund’s strong track record adds credibility, but risk management is key.

How to Invest: A Quick Guide

Ready to dip your toes in? Here’s a simple step-by-step:

- Choose a Platform: Use SBI Mutual Fund’s website, apps like Groww, or a financial advisor.

- Complete KYC: Submit ID proof, address proof, and PAN (one-time process).

- Select the Fund: Pick SBI Small Cap Fund (Growth or Dividend option).

- Invest: Start with a lump sum (min. ₹5,000) or SIP (min. ₹500).

- Monitor: Check performance quarterly, but avoid knee-jerk reactions.

FAQs: Your Questions Answered

What is a small-cap fund?

A small-cap fund invests in companies with small market caps (beyond India’s top 250). They aim for high growth but carry higher risks.

Is the SBI Small Cap Fund risky?

Yes, it’s high-risk due to small-cap volatility. Expect ups and downs, especially in the short term.

What’s the minimum investment?

Lump sum: ₹5,000. SIP: ₹500.

Can I invest via SIP?

Absolutely! SIPs let you invest small amounts regularly, reducing the impact of market swings.

What about taxes?

- Long-Term Capital Gains (LTCG): 12.5% on gains above ₹1.25 lakh (held >1 year).

- Short-Term Capital Gains (STCG): 20% if sold within a year.

How does it compare to other small-cap funds?

The SBI Small Cap Fund often ranks high for consistency and returns, but compare peers like Nippon India Small Cap or HDFC Small Cap for a fuller picture.

Conclusion: Hype, Truth, or Somewhere In Between?

So, can ₹1 lakh become ₹7 lakh with the SBI Small Cap Fund? It’s not hype—it’s possible, based on historical returns of 18-22% annually. At 18%, it takes ~11.5 years; at 22%, ~9.5 years. But it’s not a sure thing. Small-cap funds are volatile beasts—capable of soaring highs and stomach-churning lows. The truth lies in your ability to stay invested through market cycles, embrace risk, and think long-term.

If you’re an aggressive investor with a decade to spare, the SBI Small Cap Fund could be your ticket to significant wealth. But if you’re risk-averse or need quick cash, look elsewhere. Before you invest, do your homework or chat with a financial advisor to ensure it fits your goals. The potential is real, but so are the pitfalls. Will you take the leap?