Both save you ₹46,800 in tax under Section 80C — but one could quietly build 3× more wealth over 15 years. Here’s the unfiltered truth.

Quick AnswerELSS wins on returns and lock-in period. PPF wins on safety and tax-free income. The real winner depends entirely on your age, risk tolerance, and financial goals — and this article will show you exactly which one that is for you.

What Exactly Are You Choosing Between?

Every year, millions of Indians rush to invest before March 31st to save tax under Section 80C. The limit is ₹1.5 lakh per year — and the two most popular choices are ELSS (Equity Linked Savings Scheme) and PPF (Public Provident Fund).

They both give you the same tax deduction. But that’s where the similarity ends. One is a market-linked mutual fund. The other is a government-backed savings scheme. Choosing wrong could cost you lakhs over a decade.

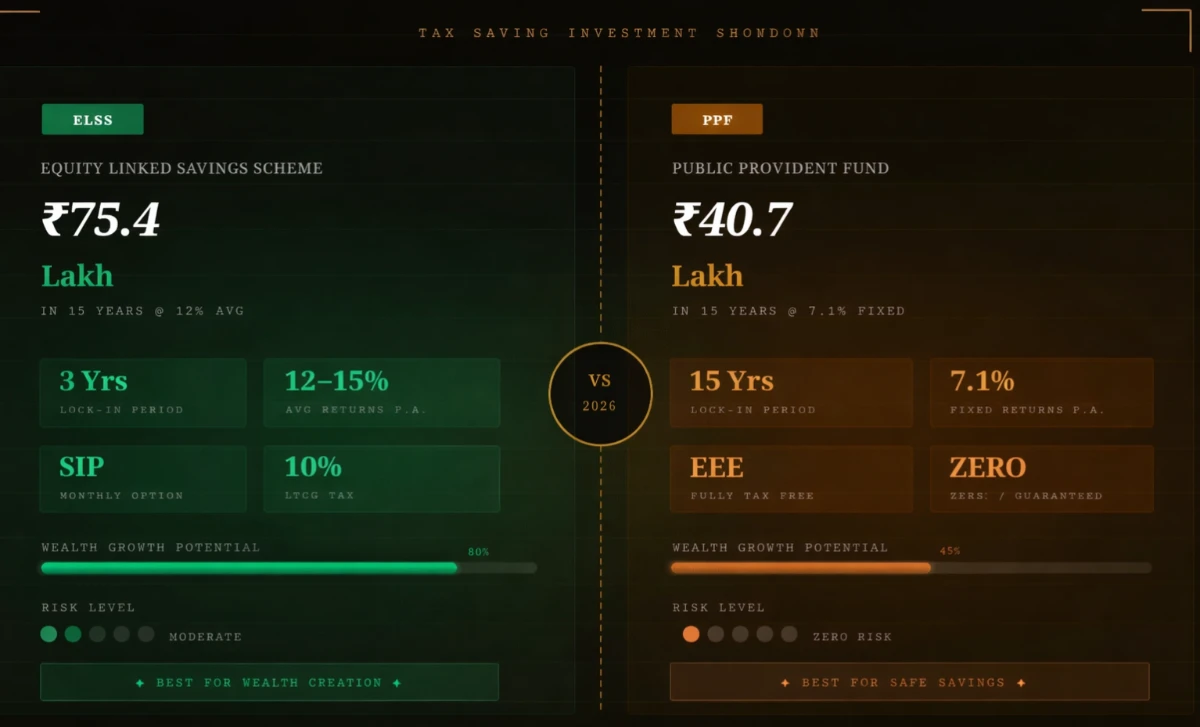

ELSS

Equity Linked Savings Scheme

- Invests in stock markets (equity)

- Lock-in: Only 3 years

- Returns: Market-linked (12–15% avg)

- Tax on gains: 10% LTCG above ₹1 lakh

- Managed by mutual fund houses

PPF

Public Provident Fund

- Government-backed fixed savings

- Lock-in: 15 years (extendable)

- Returns: ~7.1% (govt. revised quarterly)

- Tax on gains: Completely zero

- Backed by Ministry of Finance

The Full Comparison

| Parameter | ELSS | PPF |

|---|---|---|

| Lock-in Period | 3 Years ✓ Win | 15 Years |

| Average Returns | 12–15% p.a. ✓ Win | 7.1% p.a. |

| Risk Level | Moderate–High | Zero Risk ✓ Win |

| Tax on Maturity | 10% LTCG (above ₹1L) | Fully Tax-Free ✓ Win |

| Min Investment | ₹500/month ✓ Win | ₹500/year |

| Max Investment | No upper limit | ₹1.5 lakh/year |

| Loan Facility | After 3 yrs (units) | From 3rd year Tie |

| SIP Option | Yes ✓ Win | No |

| Inflation-Beating | Very likely ✓ Win | Marginally |

| 80C Deduction | Yes | Yes Tie |

| Premature Withdrawal | After 3 yrs (any time) | Only after 7 yrs (partial) |

| Best For | Wealth Creation | Safe Long-Term Savings ✓ Win |

₹1.5 Lakh/Year × 15 Years — See the Difference

Let’s invest the full 80C limit of ₹1.5 lakh per year in both instruments and see what you get after 15 years.

Wealth Comparison After 15 Years

ELSS @ 12% avg returns₹75.4 Lakh

PPF @ 7.1% fixed returns₹40.7 Lakh

Total Amount Invested₹22.5 Lakh

ELSSPPF

* ELSS returns are historical averages and not guaranteed. PPF rate subject to quarterly govt revision. LTCG tax not deducted from ELSS figure above.

ELSS gives you nearly ₹34 lakh more wealth over 15 years. Even after paying 10% LTCG tax on the gains above ₹1 lakh, ELSS still comes out significantly ahead.

“PPF gives you peace of mind. ELSS gives you purchasing power. Choose based on what keeps you up at night.”— Smartblog91 Investment Philosophy

Both Save ₹46,800/Year — But One Costs You More Later

ELSS Tax Calculation

ELSS follows the EEE structure partially: Investment is deducted under 80C (tax-free), but gains at maturity are taxed at 10% LTCG above ₹1 lakh. So if your ELSS grows by ₹5 lakh, you pay 10% on ₹4 lakh = ₹40,000 tax.

PPF Tax Calculation

PPF is a pure EEE (Exempt-Exempt-Exempt) product. Your investment, the annual interest, and the final maturity amount — all three are completely tax-free. Zero tax at any stage.

However, even after paying LTCG tax on ELSS, the post-tax returns of ELSS (~10.5–13.5%) still beat PPF’s 7.1% by a wide margin over long periods.

Who Should Pick What?

Choose ELSS If You…

- Are below 45 years of age

- Have a 5–10 year investment horizon

- Can handle market ups and downs

- Want maximum wealth creation

- Already have some emergency fund

- Prefer flexibility (exit after 3 yrs)

Choose PPF If You…

- Are 50+ or nearing retirement

- Cannot afford to lose capital

- Want guaranteed, predictable income

- Are in the highest 30% tax bracket

- Need a completely tax-free corpus

- Prefer government-backed security

The Real Winner: Use Both Together

Smart investors don’t choose one over the other. They split the ₹1.5 lakh limit strategically based on their age and goals:

If You’re Under 40

Put ₹1 lakh in ELSS (via monthly SIP of ₹8,333) and ₹50,000 in PPF. You get equity-driven growth on the bulk while maintaining a guaranteed, tax-free safety net.

If You’re 40–55

Split 50:50 — ₹75,000 each. You’re balancing growth with stability as retirement approaches. Gradually shift more to PPF each year.

If You’re 55+

Consider putting ₹1.25 lakh in PPF and just ₹25,000 in ELSS (if risk tolerance allows). Capital protection becomes more important than growth at this stage.

Final Verdict

For most working Indians below 50, ELSS is the superior tax-saving investment. The shorter lock-in, higher returns, and SIP flexibility make it a wealth-creation powerhouse.

But PPF is not obsolete. It’s the bedrock of financial safety — especially for risk-averse investors, senior citizens, and those in the 30% tax bracket who want zero tax at maturity.

Bottom line: If you’re young — lean ELSS. If you’re near retirement — lean PPF. If you’re smart — do both.

5 Things to Remember

1. ELSS has the shortest lock-in (3 years) among all 80C investments — even shorter than NPS or ULIP.

2. PPF has a 15-year lock-in but can be extended indefinitely in 5-year blocks after maturity.

3. ELSS returns are not guaranteed — in a bad market year, you could see negative returns short-term.

4. PPF interest rate is not fixed forever — it’s revised by the government every quarter and has been as low as 7.1%.

5. Both qualify for 80C deduction up to ₹1.5 lakh — so you can split between both within the same limit.