Imagine waking up every morning knowing that ₹50,000 has been deposited into your account — without you lifting a finger. No client calls, no office commute, no deadlines.

This is not a fantasy. Thousands of Indian investors already live this reality by building a smart dividend stock portfolio. And in this guide, you’ll learn exactly how to do the same — step by step, with real numbers.

What you’ll learn: How dividend investing works, how much money you need to invest, which Indian stocks pay the best dividends, and how to structure your portfolio to receive income every single month.

What Are Dividend Stocks?

When a company earns profits, it has two choices: reinvest that money back into the business, or share a portion of it with shareholders. When it chooses the second option, that payment is called a dividend.

Dividend stocks are shares of companies that regularly pay dividends to their investors. You simply buy and hold these stocks, and you receive cash payments — quarterly, semi-annually, or annually — just for being a shareholder.

Why Are Dividends Perfect for Passive Income?

Unlike capital gains (where you must sell a stock to realize profit), dividends land in your account without you selling anything. Your principal investment stays intact. This makes dividends one of the most powerful forms of truly passive, recurring income.

“Don’t work for money. Make money work for you.” — Robert Kiyosaki

How Much Corpus Do You Need to Earn ₹50,000/Month?

This is the most important question — and the answer depends on dividend yield.

Dividend Yield = (Annual Dividend per Share ÷ Current Share Price) × 100

Indian blue-chip stocks typically offer dividend yields between 1.5% and 5% per annum. Let’s calculate the required corpus at different yield levels:

₹2 CrAt 3% Yield

₹1.5 CrAt 4% Yield

₹1.2 CrAt 5% Yield

Simple Formula: Required Corpus = (Target Monthly Income × 12) ÷ Dividend Yield%

Example: (₹50,000 × 12) ÷ 0.04 = ₹1,50,00,000 (₹1.5 Crore) at 4% average yield.

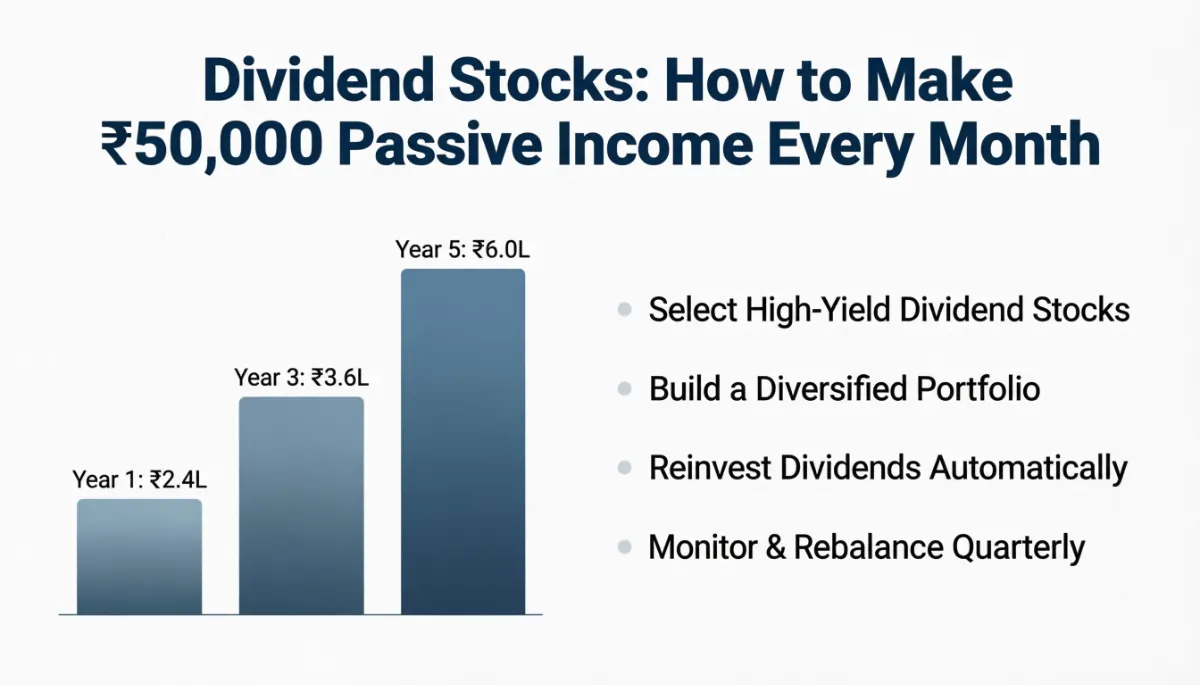

This might sound like a large number, but remember: you’re building this corpus gradually over 8–12 years through disciplined SIP-style investing in quality dividend stocks.

Best Dividend-Paying Stocks in India (2025)

Not all dividend stocks are created equal. The best dividend stocks combine a high yield with consistent dividend history and a strong balance sheet. Here are some of India’s most reliable dividend payers across sectors:

| Company | Sector | Approx. Dividend Yield | Consistency |

|---|---|---|---|

| Coal India | Energy / PSU | 5–7% | Very High |

| ONGC | Oil & Gas / PSU | 4–6% | High |

| Power Grid Corp | Utilities / PSU | 4–5% | Very High |

| ITC Limited | FMCG / Conglomerate | 3–4% | Very High |

| NHPC | Hydro Power / PSU | 4–5% | High |

| Hindustan Zinc | Metals & Mining | 5–8% | High |

| REC Limited | NBFC / Finance | 4–6% | High |

| Infosys | IT Services | 2.5–3.5% | Very High |

⚠️ Disclaimer: The above stocks are mentioned for educational purposes only. Always do your own research (DYOR) or consult a SEBI-registered financial advisor before investing. Past dividend history does not guarantee future payments.

Step-by-Step Strategy to Build Your Dividend Portfolio

- Define Your Income Goal & Timeline. Decide your target monthly income (e.g., ₹50,000) and your investment horizon. A 10-year plan is realistic for most salaried investors. Work backwards using the formula above to determine your target corpus.

- Open a Demat + Trading Account. Choose a SEBI-regulated broker like Zerodha, Groww, or HDFC Securities. Link your bank account for automatic dividend credit — dividends are deposited directly to your registered bank account by SEBI mandate.

- Screen Stocks Using the 3-Filter Method. Filter by: (1) Dividend yield above 3%, (2) Consecutive dividend payments for 5+ years, (3) Payout ratio below 70% (so the company isn’t over-distributing). Tools like Screener.in or Tickertape make this easy.

- Invest Monthly via SIP-Style Accumulation. Don’t try to invest everything at once. Invest a fixed amount every month — say ₹30,000–₹50,000 — across your chosen dividend stocks. This rupee-cost averaging strategy reduces timing risk significantly.

- Reinvest Dividends Early On (DRIP Strategy). In the early years, don’t spend the dividends — reinvest them back into the same or other dividend stocks. This compounding effect dramatically accelerates your corpus growth.

- Review Portfolio Annually. Check each company’s financial health, payout ratio, and dividend history every year. Replace any company that cuts its dividend or shows deteriorating fundamentals with a stronger alternative.

How to Diversify for Monthly Income (Not Just Annual)

One common problem with dividend investing is that most Indian companies pay dividends once or twice a year — not every month. The solution is staggered portfolio diversification.

Here’s how to structure your holdings so income arrives throughout the year:

| Quarter | Sector Focus | Strategy |

|---|---|---|

| Q1 (Jan–Mar) | IT, FMCG | Hold Infosys, HUL, ITC |

| Q2 (Apr–Jun) | PSU Banks, Energy | Hold Coal India, ONGC, SBI |

| Q3 (Jul–Sep) | Metals, Utilities | Hold Hindustan Zinc, Power Grid |

| Q4 (Oct–Dec) | Finance, NBFC | Hold REC, PFC, NHPC |

By holding stocks from sectors that declare dividends in different quarters, you effectively create a monthly income pipeline from what are technically annual or semi-annual dividends.

Tax on Dividend Income in India — What You Must Know

Since Budget 2020, the old Dividend Distribution Tax (DDT) system was abolished. Now, dividend income is taxed in the hands of the investor at their applicable income tax slab rate.

Key Tax Rules (2024–25 and 2025–26):

- Added to your income: Dividend income is added to your total income and taxed at your slab rate (5%, 20%, or 30%).

- TDS by companies: If your dividend from a single company exceeds ₹5,000 in a year, the company deducts 10% TDS before paying you.

- Form 15G/15H: If your total income is below the taxable limit, you can submit Form 15G (or Form 15H for seniors) to avoid TDS deduction.

- No LTCG benefit: Dividends are ordinary income — unlike long-term capital gains, they do not enjoy a flat 10% tax rate.

Tax Tip: If your total annual dividend income is ₹6,00,000 (₹50,000/month) and you have no other income, you’ll pay tax only on income above ₹3 lakh under the new regime, making your effective tax rate quite manageable. Consider consulting a CA to optimize your tax structure.

6 Common Mistakes Dividend Investors Make (And How to Avoid Them)

1. Chasing the Highest Yield Blindly

A 12% dividend yield sounds amazing — until the company slashes it next year. Always check the payout ratio (dividend ÷ earnings). If it’s above 80%, the dividend is likely unsustainable.

2. Ignoring Dividend Growth

A company paying ₹5/share today that grows its dividend at 10% annually is far more valuable than one paying ₹8/share with no growth. Prioritize dividend growth history, not just current yield.

3. Concentrating in a Single Sector

PSU stocks offer high yields but are subject to government policy changes. Don’t put more than 30–35% of your portfolio in any one sector.

4. Spending Dividends Too Early

In the accumulation phase (first 5–8 years), reinvesting dividends is critical. The compounding effect of reinvested dividends can contribute up to 40% of your total returns over 10 years.

5. Not Checking the Ex-Dividend Date

You must own shares before the ex-dividend date to receive the upcoming dividend. Buying after this date means you miss that payment cycle entirely.

6. Neglecting Portfolio Rebalancing

A company that was a great dividend payer three years ago may have weakened fundamentals today. Annual review and rebalancing ensures you keep only high-quality dividend payers.

Frequently Asked Questions

Can I really earn ₹50,000/month from dividend stocks?

Yes, but it requires a corpus of approximately ₹1.2–2 crore invested in stocks with a 3–5% annual yield. This is achievable through consistent long-term investing over 8–12 years.

Which is better — dividend stocks or FD for passive income?

Fixed Deposits currently offer 6.5–7.5% interest and are low-risk, but dividend stocks offer the dual benefit of dividend income plus capital appreciation. Over the long term, quality dividend stocks tend to significantly outperform FDs in total returns.

Are PSU stocks good for dividends?

Yes — PSU (Public Sector Undertaking) companies like Coal India, ONGC, and Power Grid are among India’s most consistent dividend payers with high yields. However, their stock prices can be sensitive to government policies and commodity cycles.

Do I need ₹1.5 crore right now to start?

Absolutely not. You start small and build your corpus over time. Even ₹10,000–₹20,000 per month invested consistently for 10–12 years can grow into a substantial dividend-generating portfolio through compounding.

How do I receive dividends? Do I need to do anything?

No action needed. As long as your Demat account is linked to your bank account, dividends are automatically credited to your bank account on the payment date — no selling required.

Should I invest in dividend mutual funds instead of direct stocks?

Dividend-focused mutual funds (like IDCW plans) or dividend ETFs are great alternatives for beginners who want professional management. However, the payouts are not guaranteed, and fund managers may reinvest dividends rather than distribute them. Direct stock investing gives you more control.

Final Thoughts: Your Dividend Journey Starts Today

Earning ₹50,000 every month without working is no longer a dream reserved for the ultra-wealthy. With patience, discipline, and the right dividend strategy, any Indian investor with a steady income can build this passive income machine.

The key takeaways are simple:

- Start investing in quality, high-yield dividend stocks as early as possible

- Reinvest your dividends in the early years for maximum compounding

- Diversify across sectors to smooth out income throughout the year

- Be patient — this is a 10-year game, not a 10-month shortcut

The best time to start building your dividend portfolio was 10 years ago. The second best time is today.