Quick Answer: For most salaried Indian investors, SIP is the better default because it builds discipline and averages out market volatility. Lump sum can outperform SIP only when invested at a genuine market low with a long holding period — timing most investors cannot reliably achieve.

SIP and Lump Sum: The Core Difference

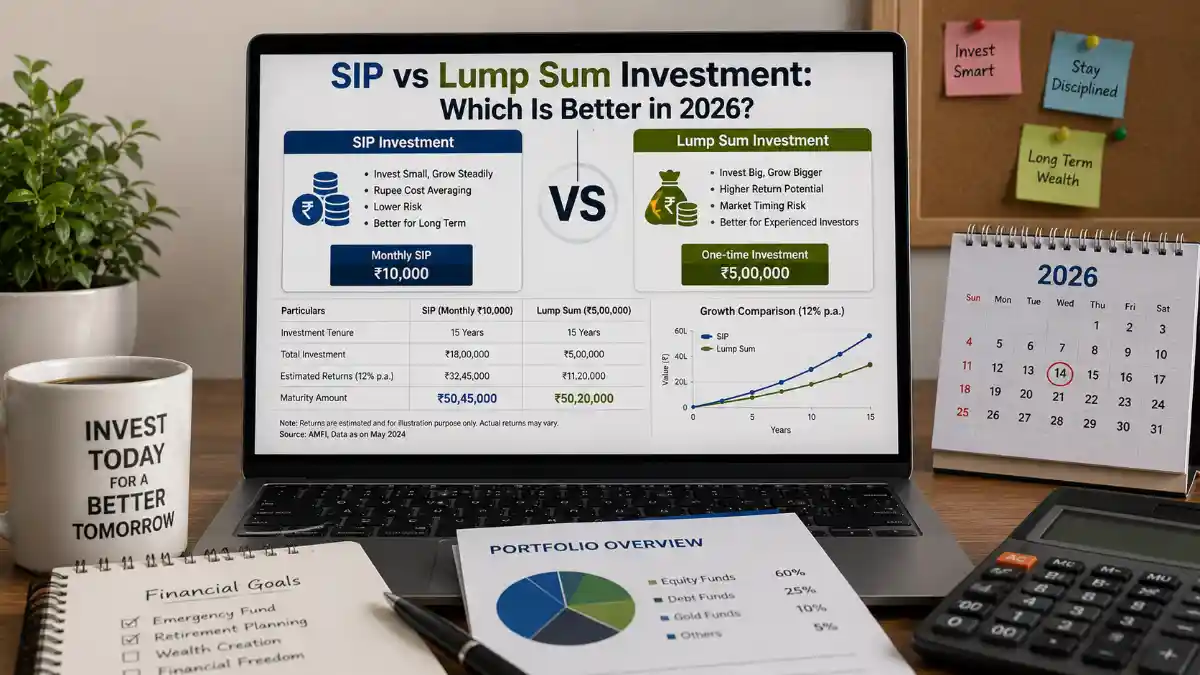

A Systematic Investment Plan (SIP) means investing a fixed amount every month into a mutual fund scheme, regardless of whether markets are up or down. A lump sum investment means putting your entire investible amount into a scheme in one go.

Both routes lead to the same destination — mutual fund units — but the journey, risk exposure, and psychological experience are very different.

What the 2026 Data Actually Shows

The debate isn’t just theoretical anymore — 2026 has given Indian investors a real stress test. Monthly SIP contributions have stayed remarkably steady, coming in around ₹31,000–32,000 crore for several months in a row, even as equity markets swung on geopolitical tension and crude oil volatility. In June 2026, SIP inflows rose to roughly ₹31,781 crore, extending a streak of collections at or near the ₹31,000 crore mark for five straight months.

Compare that to lump sum-driven net equity inflows, which are far more volatile: they fell sharply in May 2026 amid the US-Iran conflict and elevated crude prices near $90–93 a barrel, before rebounding as sentiment improved in June. This pattern is the real-world proof of the SIP argument — disciplined monthly investors kept investing straight through the volatility, while lump-sum-driven flows moved in and out based on news cycles.

SIP assets under management have also crossed ₹17 lakh crore, now making up close to 21% of the entire mutual fund industry’s AUM of over ₹81 lakh crore — a sign of how central SIPs have become to Indian retail investing.

SIP vs Lump Sum: Side-by-Side Comparison

| Parameter | SIP | Lump Sum |

|---|---|---|

| Investment style | Fixed amount monthly | One-time, full amount |

| Market timing risk | Low — averages entry price | High — depends entirely on entry point |

| Best suited for | Salaried individuals, regular income | Bonus, inheritance, matured FD, windfall |

| Volatility handling | Rupee-cost averaging cushions falls | Full exposure from day one |

| Discipline required | Built-in via auto-debit | Requires investor conviction upfront |

| Ideal market condition | Any — volatile or trending markets | Works best near a market bottom |

| Taxation on gains | Each instalment taxed separately by its own holding period | Single holding period from investment date |

When SIP Makes More Sense

- You earn a regular monthly salary and want to invest a fixed portion automatically.

- You want to reduce the emotional stress of deciding “is this the right time to invest?”

- You are investing for a long-term goal — retirement, child’s education, or wealth creation over 10+ years.

- You want your investment to automatically buy more units when markets fall and fewer when they rise.

When Lump Sum Makes More Sense

- You’ve received a bonus, gratuity, or matured fixed deposit and want to deploy it into equity markets.

- Markets have corrected meaningfully and valuations look attractive relative to history.

- You have a long investment horizon (7+ years) that can absorb short-term volatility from investing all at once.

- You’re comfortable staying invested through a temporary drawdown without panic-selling.

The Smarter Middle Path: STP

Many experienced investors use a Systematic Transfer Plan (STP) when they have a large lump sum but are nervous about deploying it all at once. The money is first parked in a liquid or debt fund, then transferred systematically into an equity fund over 6–12 months — combining the safety of averaging with the fact that idle cash still earns some return while it waits.

Our Verdict

For the vast majority of Indian retail investors, SIP remains the more reliable, behaviourally sound choice. The 2026 data makes the case clearly: even during months of geopolitical shocks and oil price spikes, SIP contributions barely wavered, while lump-sum-linked equity inflows swung by 30–40% month-on-month. That consistency is exactly what long-term compounding needs.

Lump sum investing isn’t wrong — it can deliver strong results if you invest during a genuine correction and hold for the long term. But it demands market-timing skill and emotional discipline that few investors, professional or retail, consistently get right. If you’re unsure, starting a SIP today and adding lump sums opportunistically during market dips gives you the best of both approaches.

Frequently Asked Questions

1. Is SIP always better than lump sum?

Not always, but it’s better suited to most investors because it removes the need to time the market and builds a consistent saving habit.

2. Can I do both SIP and lump sum together?

Yes. Many investors run a regular SIP for monthly savings and add lump sum investments during market corrections to boost long-term returns.

3. What is the minimum amount needed to start a SIP in India?

Most mutual funds allow SIPs starting from as low as ₹500 per month, making it accessible to nearly every investor.

4. Does lump sum investment carry more risk than SIP?

Yes, because the entire amount is exposed to market movements from day one, whereas SIP spreads that risk across multiple purchase dates.

5. Is SIP taxed differently from lump sum investment?

Yes. Each SIP instalment is treated as a separate investment for capital gains tax purposes, with its own holding period, while a lump sum has a single holding period from the date invested.