✦ Direct Answer

At 12% annual return, a ₹5,000/month SIP reaches ₹1 crore in ~26 years. At 15%, it takes ~21 years. At 18%, just ~18 years.

A SIP (Systematic Investment Plan) of ₹5,000 per month may feel modest — but combined with compounding and time, it is one of the most powerful wealth-building tools available to Indian investors. In this guide, we break down the exact timeline, show you the maths, and tell you how to reach your ₹1 crore goal faster.

Key Takeaway: You will invest just ₹15–18 lakh in total over 25+ years, yet your corpus grows to ₹1 crore or more. That gap — ₹80+ lakh — is pure compounding magic.

What Is a SIP and Why Does It Work?

A SIP (Systematic Investment Plan) is a method of investing a fixed amount in a mutual fund at regular intervals — usually monthly. Every time you invest, you buy units at the current NAV (Net Asset Value). Over time, you automatically benefit from rupee cost averaging — buying more units when markets are low and fewer when markets are high.

The real superpower of SIP is compounding: your returns generate further returns every year. Over 20–30 years, this creates an exponential curve that dwarfs your actual investment.

The SIP Formula Explained

The future value of a SIP is calculated using this standard formula:

SIP Future Value Formula

FV = P × [ ( (1 + r)ⁿ − 1 ) / r ] × (1 + r)

Where:

P = Monthly SIP amount (₹5,000)

r = Monthly return rate (Annual rate ÷ 12)

n = Total number of months

FV = Future corpus value

For example, at 12% annual return, r = 12/12/100 = 0.01. At 26 years, n = 312 months. Plugging in: FV ≈ ₹1.00 crore. Let’s now see this across all realistic return scenarios.

Years to Reach ₹1 Crore: Return-Rate Comparison Table

Below is a complete comparison of how long your ₹5,000 SIP takes to become ₹1 crore at different compounded annual growth rates (CAGR):

| Annual Return | Years to ₹1 Cr | Total Invested | Returns Earned | Fund Type |

|---|---|---|---|---|

| 6% | ~44 years | ₹26.4 lakh | ₹73.6 lakh | Debt / Liquid Fund |

| 8% | ~36 years | ₹21.6 lakh | ₹78.4 lakh | Conservative Hybrid |

| 10% | ~30 years | ₹18.0 lakh | ₹82.0 lakh | Balanced Fund |

| 12% | ~26 years | ₹15.6 lakh | ₹84.4 lakh | Large-Cap Equity |

| 15% | ~21 years | ₹12.6 lakh | ₹87.4 lakh | Flexi-Cap / Mid-Cap |

| 18% | ~18 years | ₹10.8 lakh | ₹89.2 lakh | Small-Cap / ELSS |

⭐ = Most commonly used benchmark. Returns are hypothetical based on compounding formula and historical averages. Actual returns vary. Past performance is not a guarantee of future returns.

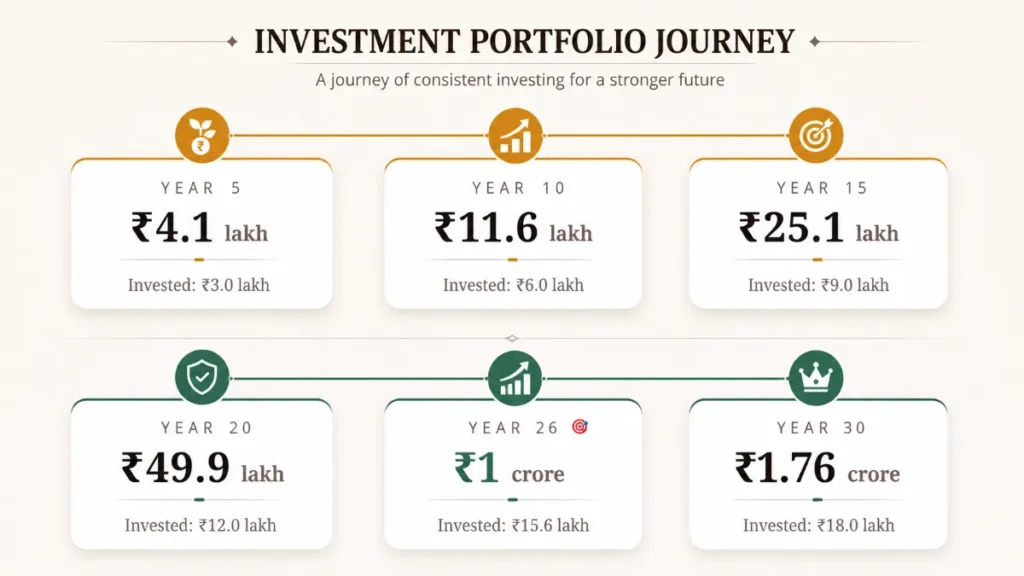

Corpus Milestones at 12% CAGR (Year-by-Year)

Here’s how your ₹5,000/month SIP grows over the years at a 12% annual return:

Notice the magic of the last 6 years: From year 20 to year 26, your corpus nearly doubles — from ₹49.9 lakh to ₹1 crore — even though you’re only adding ₹3.6 lakh more. That is compounding in action.

Strategies

How to Reach ₹1 Crore Faster

You don’t have to wait 26 years. Here are proven strategies to accelerate your timeline:

Step-Up SIP Annually

Increase your SIP by 10–15% every year as your income grows. A ₹5,000 SIP that grows 10% annually reaches ₹1 crore in just 20 years instead of 26 — saving 6 years!

Choose Higher Return Funds

Moving from a 12% large-cap fund to a 15–18% mid/small-cap fund can cut 5–8 years off your timeline. Higher risk, but historically rewarding over 15+ years.

Start Earlier

Every year you delay costs you crores. A 25-year-old starting today reaches ₹1 crore by age 51. A 30-year-old reaches it at 56. Time is your greatest asset.

Never Break the SIP

The biggest mistake investors make is pausing SIPs during market crashes. Those dip months are actually when you buy the most units — the fuel for your future returns.

Add Lump Sum on Dips

Supplement your SIP with annual bonus or windfall lump-sum investments during market corrections to dramatically reduce the timeline.

Tax-Saving ELSS Funds

ELSS funds offer up to ₹1.5 lakh deduction under Section 80C, while historically delivering 14–18% CAGR. You earn returns and save tax simultaneously.

Best Fund Categories for a ₹5,000 SIP

Here’s a quick guide to which fund type suits your risk profile and timeline:

| Fund Category | Expected CAGR | Risk Level | Best For |

|---|---|---|---|

| Large-Cap Equity | 10–13% | Moderate | Stable, long-term wealth |

| Flexi-Cap / Multi-Cap | 12–16% | Moderate-High | Best balance of growth & safety |

| Mid-Cap Equity | 14–18% | High | 10+ year horizon, higher tolerance |

| Small-Cap Equity | 15–22% | Very High | 15–20 year view, aggressive goals |

| ELSS (Tax Saving) | 13–18% | Moderate-High | Tax saving + wealth creation |

3 Mistakes That Will Delay Your ₹1 Crore Goal

1. Stopping SIP During Market Crashes

When markets fall 20–30%, many investors panic and stop their SIPs. This is the single worst decision you can make. Market downturns are when your ₹5,000 buys the most mutual fund units — and when the seeds of future wealth are planted.

2. Switching Funds Too Often

Chasing last year’s “best performing fund” destroys compounding. Every time you switch, you reset your return clock and may trigger exit loads or short-term capital gains tax. Stay invested for the long term.

3. Not Reviewing Annually

Once a year, review your SIP: Is the fund still top-quartile in its category? Has your risk tolerance changed? Should you step up the amount? An annual review keeps you on track without reactive decisions.

FAQs

How many years will it take to earn Rs 1 crore with Rs 5,000 SIP?

At 12% CAGR (historical average for equity mutual funds), it takes approximately 26 years. At 15%, about 21 years. At 18%, around 18 years.

How much will ₹5,000 SIP grow in 20 years?

At 12% CAGR, a ₹5,000 monthly SIP grows to approximately ₹49.9 lakh in 20 years. You invest only ₹12 lakh; the remaining ₹37+ lakh is pure compounding returns.

What SIP amount do I need to reach ₹1 crore in 15 years?

To reach ₹1 crore in 15 years at 12% CAGR, you need approximately ₹20,000 per month. At 15%, about ₹16,000/month.

Is SIP safe for long-term investing?

Equity mutual fund SIPs carry market risk but historically, any SIP held for 15+ years in a diversified equity fund has never delivered negative real returns in India. The longer you stay invested, the more risk reduces.

What is Step-Up SIP and how does it help?

A Step-Up SIP allows you to increase your SIP amount by a fixed percentage each year (usually 10–15%). Starting with ₹5,000 and stepping up 10% annually, you can reach ₹1 crore in just ~20 years instead of 26 — a 6-year saving!

Which is the best mutual fund for Rs 5,000 SIP?

For a ₹5,000 SIP, consider well-rated Flexi-Cap or Mid-Cap equity funds with a 5-star Morningstar rating, low expense ratio (<1%), and a proven 10-year track record. Always consult a SEBI-registered investment advisor before investing.

The Bottom Line 26 Years

A disciplined ₹5,000 SIP at 12% CAGR turns ₹15.6 lakh of your money into ₹1 crore. The secret isn’t a high income — it’s consistency, time, and never breaking the chain.

The best time to start was 10 years ago. The second-best time is today.