If you have a lump sum of ₹15 lakhs and are wondering where to invest it, this guide breaks down every major option available to Indian investors in 2026. The right investment plan depends on your risk appetite, investment horizon, and financial goals — there is no single “best” answer that fits everyone. This article covers mutual funds, PPF, fixed deposits, direct stocks, and gold, along with a risk-based allocation framework you can use to build your own plan.

Quick Note: This article is for educational purposes only. The figures used are illustrative scenarios, not guaranteed returns. Please consult a financial advisor before making investment decisions.

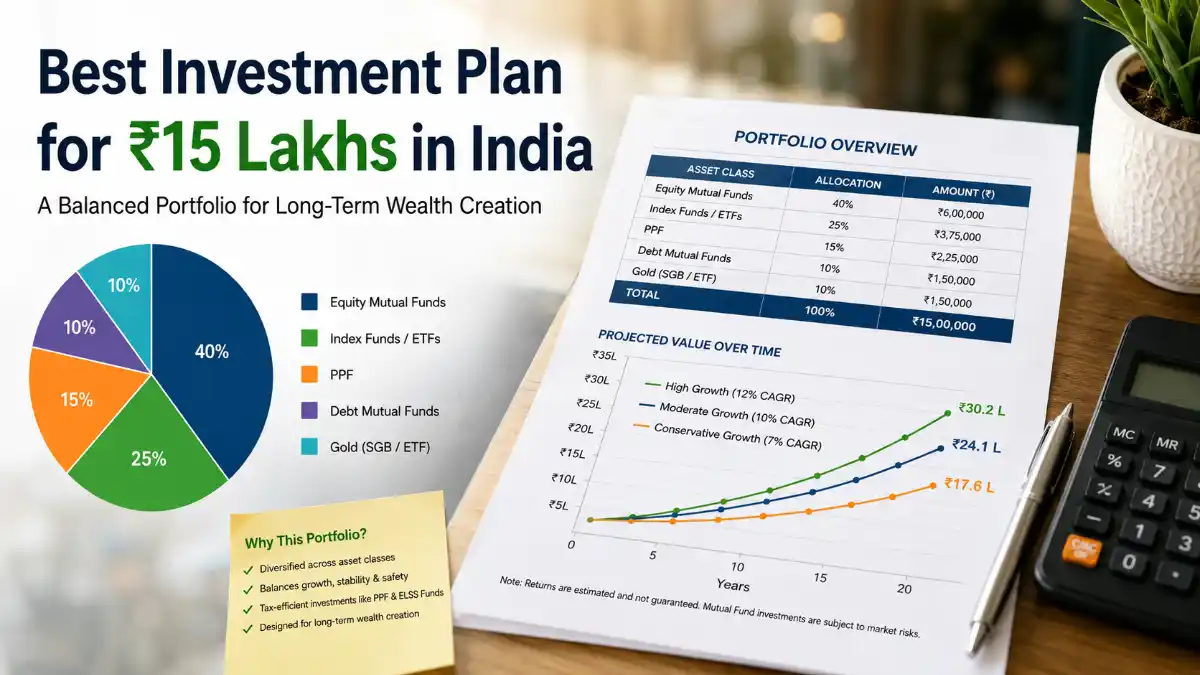

Step 1: Identify Your Risk Profile

Before allocating ₹15 lakhs, it’s important to determine whether you are a conservative, moderate, or aggressive investor. The table below outlines a general allocation framework for each profile:

| Risk Profile | Equity (Mutual Funds/Stocks) | Debt (PPF/FD/Bonds) | Gold | Suitable For |

|---|---|---|---|---|

| Conservative | 20–30% | 60–70% | 10% | Retirees, short-term goals (3-5 yrs) |

| Moderate | 45–55% | 35–45% | 10% | Balanced goals (5-10 yrs) |

| Aggressive | 65–75% | 15–25% | 10% | Long-term wealth creation (10+ yrs) |

Option 1: Mutual Funds (SIP + Lumpsum Mix)

Mutual funds are one of the most flexible options for a ₹15 lakh corpus because they offer diversification, professional fund management, and liquidity together. A common strategy is using an STP (Systematic Transfer Plan) — parking the full ₹15 lakh in a liquid fund first, then gradually transferring it into equity funds over 6-12 months. This helps reduce the risk of poor market timing.

Suggested Fund Categories

| Fund Category | Suggested Allocation | Purpose |

|---|---|---|

| Large Cap / Index Funds | 30–40% | Stability + core growth |

| Flexi Cap / Multi Cap | 25–30% | Diversified growth |

| Mid & Small Cap | 15–20% | Higher growth potential (higher risk) |

| Debt / Liquid Funds | 15–25% | Stability, emergency buffer |

Option 2: PPF (Public Provident Fund)

PPF is a government-backed, tax-free debt instrument best suited for long-term, low-risk investors. The current annual contribution limit is ₹1.5 lakh, so the entire ₹15 lakh cannot go into PPF at once — but it can form part of your debt allocation, especially if your investment horizon is 15+ years.

Option 3: Fixed Deposits (FD)

Fixed deposits are a good choice for capital protection, particularly for conservative investors or short-term goals (1-3 years). FD interest rates vary across banks and change periodically, so it’s important to check current rates directly with your bank. FD interest is fully taxable as per your income tax slab.

Option 4: Direct Stock Market Investment

If you have experience analyzing stocks and can tolerate higher risk, a portion of your ₹15 lakh (20-30% for aggressive profiles) can be allocated to direct equity in quality companies. Beginners are generally advised to start with index funds or large-cap mutual funds first, and only invest directly in stocks with money they can afford to lose.

Option 5: Gold (Digital Gold, SGBs, Gold ETFs)

Gold serves as a traditional hedge that diversifies a portfolio, especially during periods of market volatility. Sovereign Gold Bonds (SGBs), when available, tend to be the most tax-efficient option since capital gains are tax-free at maturity. A 5-10% allocation to gold is generally considered reasonable within an overall portfolio.

Illustrative Growth Scenarios (Educational Purpose Only)

The table below is a scenario-based illustration only, showing how a ₹15 lakh corpus could theoretically grow under different assumed annual growth rates. These are not predictions or guarantees — actual returns depend entirely on market conditions.

| Assumed Annual Growth | Value after 5 years | Value after 10 years | Value after 15 years |

|---|---|---|---|

| Conservative Scenario (~7%) | ~₹21.0 lakh | ~₹29.5 lakh | ~₹41.4 lakh |

| Moderate Scenario (~10%) | ~₹24.2 lakh | ~₹38.9 lakh | ~₹62.6 lakh |

| Growth Scenario (~13%) | ~₹27.6 lakh | ~₹50.9 lakh | ~₹93.8 lakh |

Key takeaway: These figures assume smooth compounding for simplicity. Real equity returns fluctuate significantly year to year and are never linear.

Tax Implications on a ₹15 Lakh Investment

| Investment Type | Tax Treatment |

|---|---|

| Equity Mutual Funds (held 1+ yr) | LTCG taxed as per current capital gains rules |

| Debt Mutual Funds | Taxed as per investor’s income slab |

| PPF | Fully tax-free (EEE status) |

| Fixed Deposit | Interest taxed as per income slab |

| Sovereign Gold Bonds | Capital gains tax-free at maturity |

Tax rules are subject to change, so always verify the latest slabs and rates on the Income Tax Department’s website or with a chartered accountant.

Disclaimer: This article is for educational and informational purposes only and does not constitute SEBI-registered investment advice. Mutual fund and stock market investments are subject to market risks — please read all scheme-related documents carefully. Consult a SEBI-registered financial advisor before making investment decisions. SmartBlog91.com and Md Adil are not liable for any investment losses.

Frequently Asked Questions

Q1. What is the safest way to invest ₹15 lakhs?

The safest approach is to diversify across low-risk instruments like PPF, fixed deposits, and debt mutual funds — especially if your goal is short-term or capital protection is your top priority.

Q2. Can I put the entire ₹15 lakhs into a single mutual fund?

It’s technically possible, but not recommended. Diversifying across fund categories — large cap, flexi cap, and debt — helps manage risk more effectively.

Q3. Is lumpsum investing better than using an STP?

If market valuations are high or you want to avoid volatility, an STP (Systematic Transfer Plan) can be a safer approach since it spreads out your average purchase cost over time.

Q4. Are guaranteed returns possible on ₹15 lakhs?

No. Only certain instruments like PPF and FDs offer fixed, guaranteed returns. Mutual funds and stocks are market-linked, and returns are never guaranteed.

Q5. What investment horizon should I plan for with ₹15 lakhs?

This depends on your financial goal. Equity-heavy investments generally require a 7-10+ year horizon so that short-term market volatility has less impact on overall returns.