The honest answer is: it depends entirely on the withdrawal rate you choose, and that single number swings your required corpus between ₹1.2 crore and ₹2 crore. Here’s the exact math, compared across three realistic SWP rates, so you know precisely what number to target.

Quick Answer

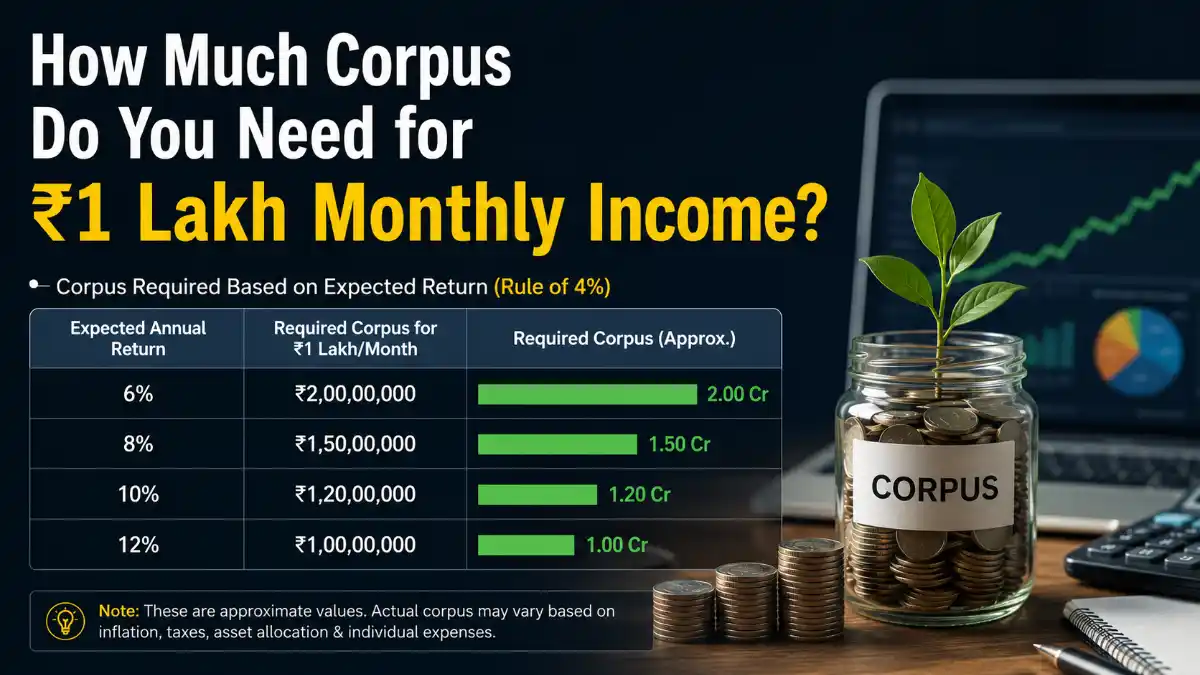

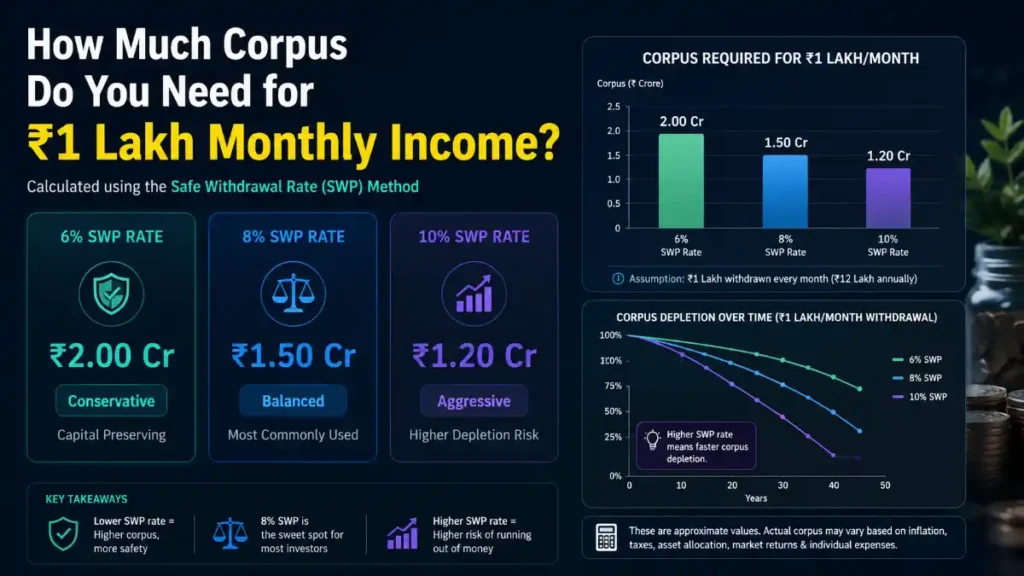

To generate ₹1 lakh per month (₹12 lakh per year) through a Systematic Withdrawal Plan, you need a mutual fund corpus of approximately ₹2 crore at a 6% annual withdrawal rate, ₹1.5 crore at 8%, or ₹1.2 crore at 10%. Lower withdrawal rates are more sustainable over 25-30 years because they let the corpus keep growing alongside your withdrawals.

The Corpus Calculation Formula

The corpus required for any target SWP income follows a simple formula:

Required Corpus = (Monthly Income × 12) ÷ Withdrawal Rate

For ₹1 lakh monthly income, the annual withdrawal amount is ₹12,00,000. Divide that by your chosen withdrawal rate (expressed as a decimal) to get the corpus.

This formula tells you the corpus needed to fund the withdrawal, but it says nothing about whether that corpus will survive the withdrawals over two or three decades. That depends on how the withdrawal rate compares to your fund’s actual returns, which we cover in the sustainability section below.

Corpus Required: 6% vs 8% vs 10% Withdrawal Rate

Here is the exact corpus needed for ₹1 lakh monthly (₹12 lakh annual) income at each withdrawal rate:

| SWP Rate | Annual Withdrawal | Corpus Required | Risk Profile |

|---|---|---|---|

| 6% | ₹12,00,000 | ₹2,00,00,000 (₹2.0 Cr) | Conservative |

| 8% | ₹12,00,000 | ₹1,50,00,000 (₹1.5 Cr) | Moderate |

| 10% | ₹12,00,000 | ₹1,20,00,000 (₹1.2 Cr) | Aggressive |

Notice the pattern: doubling the withdrawal rate from 6% to 10% only saves you about ₹80 lakh in upfront corpus, but it dramatically increases the chance your money runs out before you do. A higher withdrawal rate looks attractive on day one and becomes a problem in year fifteen.

Corpus for Different Monthly Income Targets

If ₹1 lakh isn’t your exact target, here’s how the same math scales for other common income goals:

| Monthly Income Needed | Corpus @ 6% | Corpus @ 8% | Corpus @ 10% |

|---|---|---|---|

| ₹50,000 | ₹1.00 Cr | ₹0.75 Cr | ₹0.60 Cr |

| ₹75,000 | ₹1.50 Cr | ₹1.12 Cr | ₹0.90 Cr |

| ₹1,00,000 | ₹2.00 Cr | ₹1.50 Cr | ₹1.20 Cr |

| ₹1,50,000 | ₹3.00 Cr | ₹2.25 Cr | ₹1.80 Cr |

| ₹2,00,000 | ₹4.00 Cr | ₹3.00 Cr | ₹2.40 Cr |

Does the Corpus Actually Last? A 25-Year Reality Check

The formula above tells you the starting corpus, but the real question is whether that corpus survives decades of monthly withdrawals while inflation pushes your expenses higher every year. The answer depends on a single comparison: your withdrawal rate versus your portfolio’s average annual return.

Here’s what happens to each corpus size over a 25-year SWP, assuming the underlying equity mutual fund portfolio earns a steady average return:

| Scenario | Starting Corpus | Balance After 25 Years | Outcome |

|---|---|---|---|

| 6% SWP, 12% avg. return | ₹2.00 Cr | ≈ ₹17.1 Cr | Corpus grows |

| 8% SWP, 12% avg. return | ₹1.50 Cr | ≈ ₹8.6 Cr | Corpus grows |

| 8% SWP, 10% avg. return | ₹1.50 Cr | ≈ ₹3.9 Cr | Corpus grows slowly |

| 10% SWP, 12% avg. return | ₹1.20 Cr | ≈ ₹3.5 Cr | Corpus grows slowly |

| 10% SWP, 10% avg. return | ₹1.20 Cr | ≈ ₹0.7 Cr | Eroding |

| 10% SWP, 8% avg. return | ₹1.20 Cr | ≈ ₹0.03 Cr | Nearly depleted |

The pattern is unmistakable: a 6-8% withdrawal rate gives your corpus room to grow even after two and a half decades of withdrawals, as long as the portfolio earns reasonable equity-like returns. A 10% withdrawal rate only works if returns stay consistently at or above 10-12%, and it leaves almost no margin if markets underperform for a few years, which they regularly do.

Important Caveat

These projections assume a constant average annual return, but real markets don’t move in a straight line. Sequence-of-returns risk, meaning a market downturn in the early years of your SWP, can deplete a corpus far faster than these averages suggest, even if long-term returns eventually match the assumption. This is why many planners recommend starting with a 6-7% withdrawal rate rather than pushing to 10%.

Which Withdrawal Rate Should You Choose?

There’s no single “correct” rate, but here’s how to think about it based on your situation:

- Choose 6% if your SWP needs to last 30+ years, if you have no other income source, or if you want the corpus to also serve as a legacy/inheritance amount.

- Choose 8% if you have a moderate time horizon (20-25 years), some flexibility to reduce withdrawals in bad years, or a secondary income source like rental income or a pension.

- Choose 10% or higher only if your time horizon is shorter (10-15 years), you’re comfortable with corpus depletion by design, or you have other large assets to fall back on.

A practical middle path many investors in India use: start the SWP at 7-8% of the corpus, and review the withdrawal amount every year against actual portfolio performance rather than locking it on autopilot for 25 years.

Tax Treatment of SWP Withdrawals

Every SWP installment is a partial redemption of mutual fund units, not interest income, so it gets taxed under capital gains rules rather than as regular income. Under the Budget 2024 capital gains framework:

- Equity mutual funds: Long-term capital gains (units held over 12 months) above ₹1.25 lakh per financial year are taxed at 12.5%. Short-term gains (under 12 months) are taxed at 20%.

- Debt mutual funds: Gains are added to your income and taxed at your applicable income tax slab rate, regardless of how long you held the units.

- Only the gains portion is taxed, not the entire withdrawal amount. This is why SWP is often more tax-efficient than an FD’s fully taxable interest, especially for equity-oriented SWPs in the early years.

Common Mistakes While Planning SWP Corpus

- Ignoring inflation: ₹1 lakh today won’t buy the same goods in 15 years. Many investors forget to build in a step-up withdrawal (increasing the monthly amount by 5-6% annually) to keep pace with rising costs.

- Choosing the withdrawal rate based on the highest number, not sustainability: A 10% rate gets you to your goal with a smaller corpus, but it’s the corpus lasting 25-30 years that actually matters, not just hitting the starting number.

- Assuming a single average return for the entire period: Real portfolios go through multi-year drawdowns. Stress-testing your SWP against a few bad years early on, not just a flat average, gives a more realistic picture.

- Withdrawing from a single equity fund: Most planners suggest a hybrid approach, keeping 2-3 years of withdrawals in a liquid or debt fund so you’re not forced to redeem equity units during a market downturn.

Frequently Asked Questions

How much corpus is needed for ₹1 lakh monthly income from SWP?

You need roughly ₹2 crore at a 6% annual withdrawal rate, ₹1.5 crore at 8%, or ₹1.2 crore at 10%. The lower the withdrawal rate, the longer your corpus lasts and the more room it has to keep growing alongside withdrawals.

What withdrawal rate is safe for a 25-30 year SWP?

A 6-8% annual withdrawal rate is generally considered sustainable for a 25-30 year horizon when the underlying portfolio earns 10-12% average annual returns, since the corpus can continue growing even after withdrawals. A 10% withdrawal rate works only if returns consistently exceed 10%; otherwise the corpus depletes faster.

Is SWP income from mutual funds tax-free?

No. Each SWP withdrawal is treated as a partial redemption and taxed under capital gains rules. Under Budget 2024 rules, equity fund LTCG above ₹1.25 lakh per year is taxed at 12.5%, while STCG is taxed at 20%. Debt fund gains are taxed at your income slab rate regardless of holding period.

Does the corpus run out if I withdraw 8% every year?

Not necessarily. If the underlying fund averages 10-12% annual returns while you withdraw 8%, the corpus continues to grow over time despite withdrawals. The corpus only depletes when the withdrawal rate consistently exceeds the portfolio’s average return rate.