Millions of Indian retirees face the same question: where to park a lump sum so it pays reliable monthly income — without eroding capital or losing to inflation. Two instruments dominate this conversation — SWP (Systematic Withdrawal Plan) from mutual funds, and Post Office Monthly Income Scheme (MIS). This article breaks down both in complete detail to help you choose right.

Quick Verdict

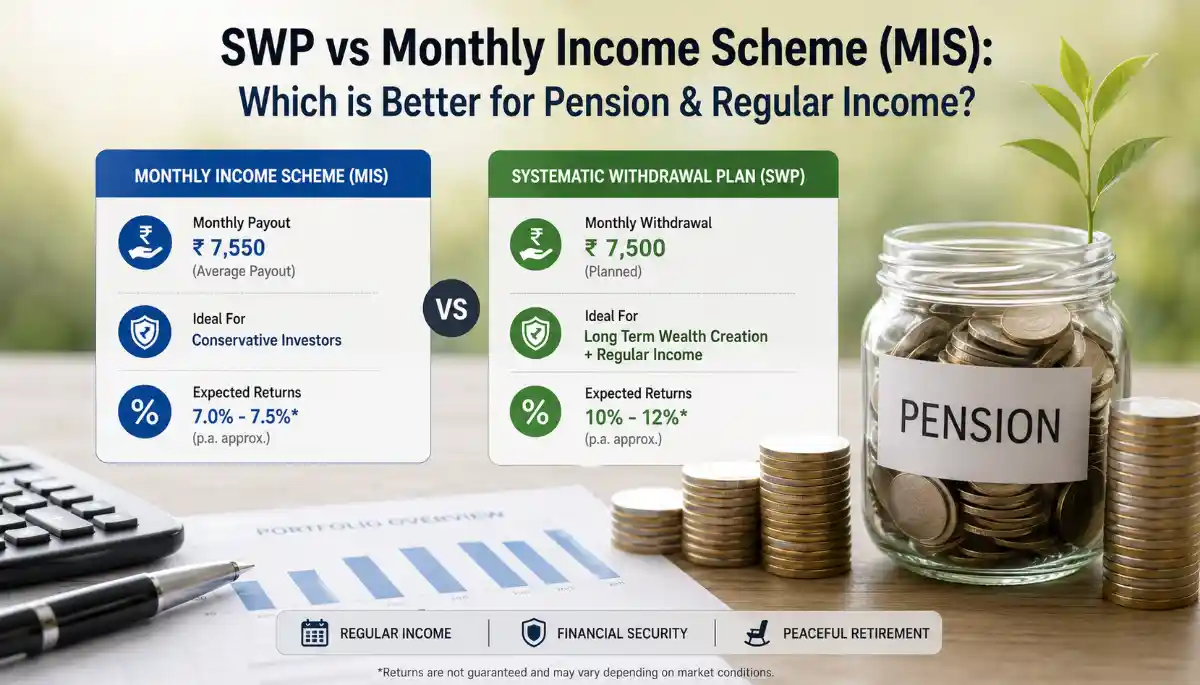

SWP

Best for Inflation-Beating Growth

Ideal if you have a 7+ year horizon, moderate risk tolerance, and want your corpus to grow while withdrawing monthly income. Tax-efficient for investors in higher tax brackets.

Post Office MIS

Best for Guaranteed Safe Income

Ideal for very conservative investors, senior citizens who need certainty, or as a debt portion of a hybrid income strategy. Zero default risk, government-backed.

What is SWP and What is Post Office MIS?

Systematic Withdrawal Plan (SWP)

A Systematic Withdrawal Plan (SWP) is a feature offered by mutual funds that allows investors to withdraw a fixed amount from their invested corpus every month (or quarterly). You invest a lump sum in a mutual fund scheme — typically a hybrid fund, debt fund, or balanced advantage fund — and set a fixed monthly withdrawal amount. The fund redeems the equivalent number of units from your account each month.

For example, if you invest ₹25 lakh in a balanced advantage fund and set a monthly SWP of ₹15,000, the fund will redeem units worth ₹15,000 every month and credit the amount to your bank account. If the fund grows at 10% CAGR, your corpus may actually increase over time even while you withdraw.

Key Insight: In a well-structured SWP, if the fund’s annual return rate exceeds the annual withdrawal rate, your corpus grows — giving you a self-replenishing income stream that beats inflation over time.

Post Office Monthly Income Scheme (MIS)

The Post Office Monthly Income Scheme (MIS) is a government savings scheme operated by India Post under the Ministry of Finance. You deposit a lump sum, and the post office pays you a fixed monthly interest on your deposit. The principal is returned at maturity (5 years). The current interest rate is 7.4% per annum (as of Q1 2025).

Maximum investment limit: ₹9 lakh (single account) and ₹15 lakh (joint account). It is one of the safest income instruments available in India as it is fully backed by the Government of India.

Note: Post Office MIS interest rates are reviewed quarterly by the government and can change. However, once you open an account, your rate is locked for the 5-year tenure.Key Feature Comparison: SWP vs Post Office MIS

Table 1: SWP vs Post Office MIS — At a Glance

| Parameter | SWP (Mutual Fund) | Post Office MIS |

|---|---|---|

| Type | Market-linked investment | Fixed income savings scheme |

| Backed by | Mutual fund assets | Government of India |

| Returns | 10–12% CAGR (equity/hybrid) | 7.4% p.a. (fixed) |

| Income Guarantee | No — market-linked | Yes — fully guaranteed |

| Minimum Investment | ₹5,000 (varies by fund) | ₹1,000 |

| Maximum Investment | No upper limit | ₹9L (single) / ₹15L (joint) |

| Tenure / Lock-in | No lock-in (except ELSS) | 5 years (premature penalty applies) |

| Liquidity | High — redeem anytime | Low — penalties for early exit |

| Inflation Protection | High (equity-linked growth) | Moderate (fixed rate) |

| Risk Level | Moderate (hybrid/balanced) | Negligible |

| Corpus Growth Potential | Yes — corpus can grow | No — corpus stays fixed |

| Tax Efficiency | High (LTCG advantages) | Low (fully taxable income) |

| Ease of Setup | Online — via fund house or app | In-person at Post Office |

| Best For | Long-term income seekers | Conservative/senior investors |

Returns & Monthly Income Calculation

Let’s understand how much monthly income each instrument generates for a given corpus. We’ll compare both at ₹9 lakh (MIS limit) and ₹25 lakh (a common retirement corpus).

Table 2: Monthly Income Comparison for ₹9 Lakh Investment

| Instrument | Investment | Rate/Return | Monthly Income | Annual Income | Tax Impact* |

|---|---|---|---|---|---|

| Post Office MIS | ₹9,00,000 | 7.4% p.a. | ₹5,550 | ₹66,600 | As per slab |

| SWP – Debt Fund | ₹9,00,000 | 7–8% p.a. | ₹5,250–6,000 | ₹63,000–72,000 | As per slab |

| SWP – Hybrid Fund | ₹9,00,000 | 10–11% p.a. | ₹7,500–8,250 | ₹90,000–99,000 | LTCG 12.5% |

| SWP – Equity Fund | ₹9,00,000 | 11–13% p.a. | ₹8,250–9,750 | ₹99,000–1,17,000 | LTCG 12.5% |

*Assumes long-term holding. Returns are illustrative based on historical category averages. Not guaranteed.

Table 3: Monthly Income for ₹25 Lakh Corpus

| Instrument | Monthly Income | Annual Income | After-Tax Income* | Corpus After 10 Yrs |

|---|---|---|---|---|

| Post Office MIS (max ₹15L + ₹10L FD) | ₹15,833 | ₹1,90,000 | ₹1,52,000 (30% slab) | ₹25,00,000 (unchanged) |

| SWP – Balanced Advantage Fund | ₹18,000–20,000 | ₹2,16,000–2,40,000 | ₹2,00,000+ (LTCG) | ₹28–32 lakh (growing) |

*Indicative only. Actual returns depend on fund performance, market conditions, and individual tax slab.

Tax Treatment: SWP vs Post Office MIS

Tax treatment is often where SWP wins decisively over Post Office MIS, especially for investors in the 20–30% income tax bracket.

Table 4: Tax Comparison — SWP vs Post Office MIS

| Tax Aspect | Post Office MIS | SWP (Equity/Hybrid Fund) | SWP (Debt Fund) |

|---|---|---|---|

| Nature of Income | Interest income — fully taxable | Capital gains (partly return of capital) | Capital gains |

| Tax Rate | As per income slab (5–30%) | LTCG 12.5% (over ₹1.25L/year) | As per income slab |

| TDS Applicability | Yes — 10% TDS (if interest > ₹40,000) | No TDS on redemptions | No TDS on redemptions |

| Principal Taxable? | No (returned at maturity) | Only gain component taxed | Only gain component taxed |

| LTCG Exemption | Not applicable | ₹1.25 lakh/year exempt | Not applicable (slab-based) |

| Effective Tax for 30% bracket | ~30% | ~12.5% (on gains only) | ~30% |

SWP Tax Advantage Explained: When you redeem units via SWP, each withdrawal consists of two parts — return of original capital (not taxable) and capital gains (taxable). If you invested ₹25 lakh and the NAV has grown 20%, only the 20% gain portion of each withdrawal is taxable — and at the concessional LTCG rate of 12.5% (after the ₹1.25 lakh annual exemption). This results in significantly lower effective tax compared to MIS where 100% of the monthly payment is taxable as interest income.

Risk Analysis: Which is Safer?

SWP — Advantages

- Corpus can grow beyond withdrawal

- Inflation-beating potential returns

- High liquidity — exit anytime

- Tax-efficient for higher-bracket investors

- No investment ceiling

- Wide choice of fund categories

SWP — Disadvantages

- Returns not guaranteed

- Market downturns can erode corpus

- Sequence-of-returns risk in early years

- Requires monitoring and discipline

- Emotional stress in volatile markets

Post Office MIS — Advantages

- 100% Government of India guarantee

- Fixed, predictable monthly income

- No market risk whatsoever

- Simple — no monitoring required

- Great for elderly / risk-averse investors

Post Office MIS — Disadvantages

- Investment cap of ₹15L (joint)

- 5-year lock-in with exit penalty

- Rate can change after renewal

- Fully taxable as interest income

- Corpus doesn’t grow — no inflation hedge

- TDS deduction (>₹40,000)

Corpus Growth Projection: 2025–2035

This is where SWP demonstrates its most powerful advantage — the self-compounding nature of a well-calibrated withdrawal rate against a growing corpus.

Table 5: Corpus Value Over 10 Years — ₹25 Lakh Investment (Monthly Withdrawal: ₹15,000)

| Year | SWP Corpus (10% CAGR) | SWP Corpus (12% CAGR) | MIS Corpus (Fixed) | MIS Cumulative Income Paid |

|---|---|---|---|---|

| 2025 (Start) | ₹25,00,000 | ₹25,00,000 | ₹25,00,000 | — |

| 2026 | ₹25,80,000 | ₹26,40,000 | ₹25,00,000 | ₹1,80,000 |

| 2027 | ₹26,64,000 | ₹27,93,000 | ₹25,00,000 | ₹3,60,000 |

| 2028 | ₹27,54,000 | ₹29,55,000 | ₹25,00,000 | ₹5,40,000 |

| 2029 | ₹28,49,000 | ₹31,29,000 | ₹25,00,000 | ₹7,20,000 |

| 2030 | ₹29,49,000 | ₹33,13,000 | ₹25,00,000 | ₹9,00,000 |

| 2031 | ₹30,56,000 | ₹35,10,000 | ₹25,00,000 | ₹10,80,000 |

| 2032 | ₹31,67,000 | ₹37,17,000 | ₹25,00,000 | ₹12,60,000 |

| 2033 | ₹32,85,000 | ₹39,37,000 | ₹25,00,000 | ₹14,40,000 |

| 2034 | ₹34,09,000 | ₹41,70,000 | ₹25,00,000 | ₹16,20,000 |

| 2035 | ₹35,38,000 | ₹44,16,000 | ₹25,00,000 | ₹18,00,000 |

MIS monthly income assumed at ₹15,000 (for a ₹24.3L investment at 7.4%). SWP projections are illustrative based on assumed CAGR. Actual returns will vary.

Key Insight: After 10 years, the SWP investor at 10% CAGR has a corpus of ₹35.38 lakh — ₹10.38 lakh more than the starting amount — while having withdrawn ₹18 lakh in income. The MIS investor’s corpus stays flat at ₹25 lakh throughout. This growing corpus is SWP’s most compelling long-term advantage.

Who Should Choose SWP and Who Should Choose MIS?

Choose SWP If You Are…

- Age 45–65 with 10+ year investment horizon

- In the 20% or 30% income tax bracket

- Investing more than ₹15 lakh (above MIS limit)

- Comfortable with moderate market volatility

- Seeking inflation-beating income growth

- Willing to monitor portfolio periodically

- Looking for flexible, no-lock-in instrument

- Wanting corpus growth alongside income

Choose Post Office MIS If You Are…

- Senior citizen (70+) with no income backup

- In the 0–5% income tax bracket

- Extremely risk-averse, prioritize capital safety

- Investing only up to ₹9–15 lakh

- Someone who cannot manage funds actively

- Looking for “set and forget” income stream

- Supplementing pension with risk-free income

- Using MIS as debt allocation in hybrid strategy

The Smart Hybrid Strategy: Combine Both

For most retirees in India, the ideal approach is not choosing one over the other — but strategically combining both to maximize safety and returns. Here’s a proven framework:

Table 6: Hybrid Income Strategy for ₹50 Lakh Retirement Corpus

| Allocation | Instrument | Amount | Monthly Income | Purpose |

|---|---|---|---|---|

| 30% | Post Office MIS (joint) | ₹15,00,000 | ₹9,250 | Guaranteed base income |

| 40% | SWP – Balanced Advantage Fund | ₹20,00,000 | ₹14,000–16,000 | Growth + inflation-beating income |

| 20% | SWP – Conservative Hybrid Fund | ₹10,00,000 | ₹6,000–7,500 | Moderate income with stability |

| 10% | Liquid Fund (Emergency Buffer) | ₹5,00,000 | As needed | Liquidity reserve |

| Total | Diversified Portfolio | ₹50,00,000 | ₹29,250–32,750/mo | Safety + Growth + Liquidity |

Why This Works: The MIS component provides a guaranteed income floor — covering essential monthly expenses no matter what markets do. The SWP components provide growth, beating inflation over the long term. The liquid fund buffer prevents forced redemptions during market downturns. This is the same principle used by institutional retirement fund managers globally.

Conclusion: SWP or Post Office MIS — The Final Verdict

There is no universal “better” option — the right choice depends entirely on your age, risk tolerance, tax bracket, income requirements, and investment horizon. Here’s the distilled verdict:

Choose Post Office MIS if you need a simple, zero-risk, guaranteed monthly income — especially if you are 70+, in a low tax bracket, and want complete peace of mind without monitoring investments.

Choose SWP (Hybrid/Balanced Fund) if you are under 70, have a 10+ year horizon, want to beat inflation, and benefit from the tax efficiency of LTCG. SWP’s ability to grow your corpus while generating income is a genuinely powerful advantage that MIS cannot replicate.

The smartest approach for most Indian retirees is a hybrid strategy — use Post Office MIS (up to ₹15 lakh joint) as your guaranteed income foundation, and supplement with SWP from balanced/hybrid funds for inflation-adjusted growth. Together, they provide both security and growth — the two things every retiree needs.