You invest just Rs 10,000 every month, and in 10 years, you’re sitting on a fortune of Rs 7 crore. Sounds like a dream, right? It’s the kind of promise that grabs attention and sparks hope—especially for those looking to build wealth without a massive upfront investment. But is it actually possible? In this deep dive into the world of Systematic Investment Plans (SIPs), we’ll uncover the truth behind this bold claim, explore the real power of a Rs 10,000 SIP, and set realistic expectations for what you can achieve.

What Is a SIP and Why Is It So Popular?

A Systematic Investment Plan (SIP) is a simple yet powerful way to invest in mutual funds. Instead of dumping a lump sum into the market, you invest a fixed amount—like Rs 10,000—regularly, usually every month. This money buys units of a mutual fund based on its Net Asset Value (NAV) at the time of investment. Over time, your wealth grows as the fund’s value rises, fueled by market performance and the magic of compounding.

In India, SIPs have become a go-to wealth-building tool for millions. Why? Because they’re accessible, flexible, and perfect for anyone who wants to save without feeling the pinch. You don’t need to be a millionaire to start—just a few hundred rupees a month can kick things off. Plus, SIPs take the stress out of timing the market, making them ideal for busy professionals, young earners, and even retirees.

But can a modest Rs 10,000 monthly SIP really turn into Rs 7 crore in just 10 years? Let’s crunch the numbers and find out.

Can a Rs 10,000 SIP Really Get You Rs 7 Crore in 10 Years?

The promise of Rs 7 crore in a decade sounds incredible, but let’s test its feasibility. To figure this out, we’ll use the future value formula for SIPs:

FV = P × [((1 + r)^n – 1) / r]

Where:

- FV = Future Value (Rs 7,00,00,000)

- P = Monthly Investment (Rs 10,000)

- r = Monthly rate of return

- n = Number of months (10 years × 12 = 120)

We need to find the annual return rate (R) that makes this equation work. Since SIPs involve monthly investments, the monthly rate (r) relates to the annual rate (R) as: r = (1 + R)^(1/12) – 1.

The Math Behind the Magic

Let’s set up the equation:

- Rs 7,00,00,000 = Rs 10,000 × [((1 + r)^120 – 1) / r]

- Divide both sides by 10,000: 7,000 = [((1 + r)^120 – 1) / r]

Now, we need to solve for r, the monthly rate, and convert it to an annual rate. This equation is tricky to solve directly, so let’s test some annual return rates and see what happens.

Testing Realistic Returns

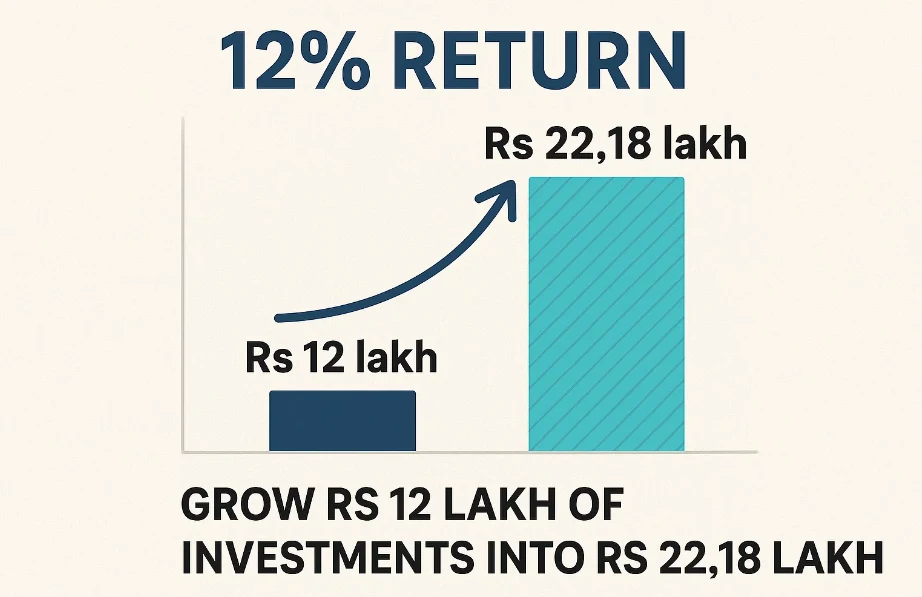

- 12% Annual Return (Common for Equity Funds):

- Monthly rate (r) ≈ (1 + 0.12)^(1/12) – 1 ≈ 0.009488

- FV = 10,000 × [((1 + 0.009488)^120 – 1) / 0.009488]

- (1 + 0.009488)^120 ≈ 3.105

- FV ≈ 10,000 × 221.8 ≈ Rs 22.18 lakh

- 15% Annual Return (Optimistic but Possible):

- Monthly rate (r) ≈ (1 + 0.15)^(1/12) – 1 ≈ 0.01171

- FV = 10,000 × [((1 + 0.01171)^120 – 1) / 0.01171]

- (1 + 0.01171)^120 ≈ 4.045

- FV ≈ 10,000 × 275.4 ≈ Rs 27.54 lakh

- 30% Annual Return (Very High):

- Monthly rate (r) ≈ (1 + 0.3)^(1/12) – 1 ≈ 0.022096

- FV = 10,000 × [((1 + 0.022096)^120 – 1) / 0.022096]

- (1 + 0.022096)^120 ≈ 13.78

- FV ≈ 10,000 × 578 ≈ Rs 57.8 lakh

Even at an impressive 30% annual return—which is rare and unsustainable over a decade—we’re nowhere near Rs 7 crore. So, what return do we actually need?

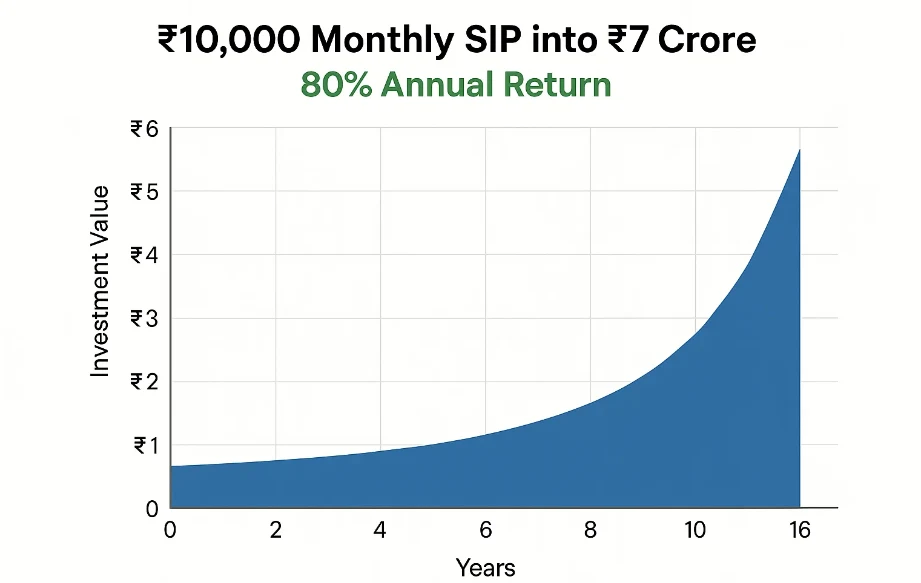

Finding the Required Return

To hit Rs 7 crore:

- 7,000 = [((1 + r)^120 – 1) / r]

- After testing higher rates, an annual return of around 80% gets us close:

- R = 80% → r ≈ 0.0504

- (1 + 0.0504)^120 ≈ 357

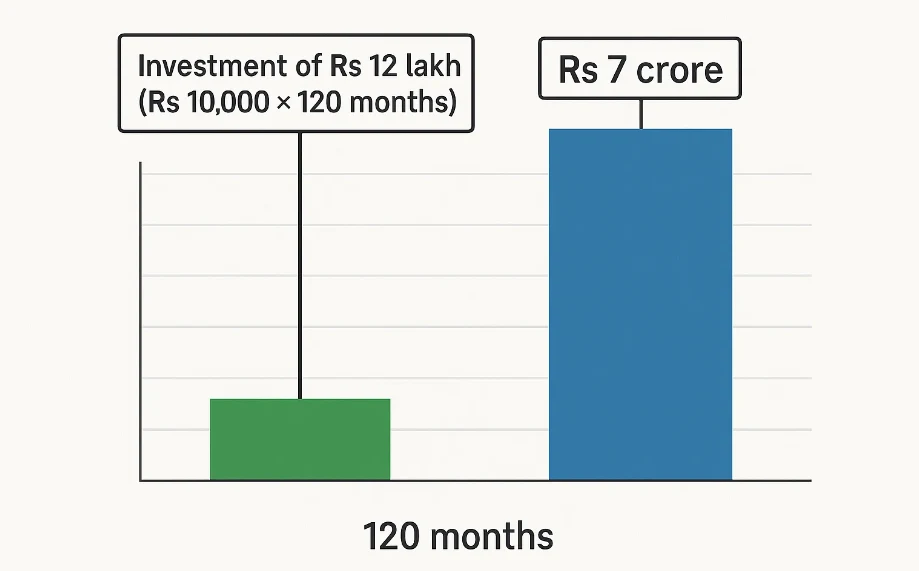

- FV ≈ 10,000 × 7,063 ≈ Rs 7.06 crore

Verdict: You’d need an astonishing 80% annual return—consistently for 10 years—to turn a Rs 10,000 monthly SIP into Rs 7 crore. Is that realistic? Not really. Historically, Indian equity markets average 12-15% annually over the long term, with top mutual funds occasionally hitting 20-25%. An 80% return year after year is more fantasy than finance.

The Real Power of a Rs 10,000 SIP: Realistic Goals

While Rs 7 crore in 10 years is out of reach with a Rs 10,000 SIP, that doesn’t mean SIPs aren’t powerful. Let’s explore what you can achieve with realistic expectations.

What You Can Expect in 10 Years

Here’s a table showing the future value of a Rs 10,000 monthly SIP over 10 years at different annual returns:

| Annual Return | Future Value (10 Years) | Key Takeaway |

|---|---|---|

| 8% | Rs 18.20 lakh | Safe, conservative growth |

| 10% | Rs 20.47 lakh | Balanced, achievable target |

| 12% | Rs 22.18 lakh | Realistic for equity funds |

| 15% | Rs 27.54 lakh | Optimistic but possible |

With a 12% return—a benchmark for equity mutual funds in India—you’d accumulate Rs 22.18 lakh in 10 years. That’s over 18 times your total investment of Rs 12 lakh (Rs 10,000 × 120 months). Not Rs 7 crore, but still a fantastic result for a modest monthly commitment!

The Long-Term Game: Stretch It to 20 or 30 Years

Time is your biggest ally in wealth creation. Let’s see how a Rs 10,000 SIP grows over longer periods:

| Tenure | 8% p.a. | 10% p.a. | 12% p.a. | 15% p.a. |

|---|---|---|---|---|

| 10 Years | Rs 18.20 lakh | Rs 20.47 lakh | Rs 22.18 lakh | Rs 27.54 lakh |

| 20 Years | Rs 53.86 lakh | Rs 72.60 lakh | Rs 98.93 lakh | Rs 1.58 crore |

| 30 Years | Rs 1.14 crore | Rs 1.81 crore | Rs 2.94 crore | Rs 5.56 crore |

- At 12% over 20 years, you’re at Rs 98.93 lakh—just shy of a crore!

- Stretch it to 30 years at 15%, and you hit Rs 5.56 crore.

While Rs 7 crore in 10 years is a stretch, Rs 5-6 crore in 30 years is entirely doable with disciplined investing and realistic returns. That’s the real power of SIPs: consistency and time.

Why SIPs Are a Wealth-Building Superpower

SIPs aren’t about overnight riches—they’re about steady, smart growth. Here’s why they’re so effective:

- Rupee Cost Averaging: You buy more units when prices dip and fewer when they rise, smoothing out market volatility.

- Compounding Magic: Your returns earn returns, snowballing your wealth over time.

- Discipline: Monthly investments keep you on track, no excuses.

- Low Entry Barrier: Start with as little as Rs 500—Rs 10,000 is just a sweet spot.

- No Timing Stress: Forget predicting market highs and lows—SIPs work regardless.

As Warren Buffett famously said, “The stock market is a device for transferring money from the impatient to the patient.” SIPs embody that patience, turning small steps into giant leaps.

How to Maximize Your Rs 10,000 SIP

Want to make the most of your SIP? Here’s how:

1. Start Early

Every year you delay costs you big. A 25-year-old starting a Rs 10,000 SIP at 12% could have Rs 2.94 crore by 55. Wait till 35, and it’s just Rs 98.93 lakh—a Rs 2 crore difference!

2. Choose the Right Fund

- Equity Funds: Higher risk, higher returns (12-15% average).

- Hybrid Funds: Mix of equity and debt for balanced growth (8-10%).

- ELSS Funds: Tax-saving with decent returns (10-12%).

Research funds with a strong 5-10 year track record and low expense ratios.

3. Increase Your SIP Over Time

Got a raise? Bump up your SIP. Even a 5-10% annual step-up can double your corpus over decades.

4. Stay Invested

Markets will dip—don’t panic. The longer you stay, the more you gain.

Expert Insights: What the Pros Say

- Benjamin Graham, the father of value investing, noted: “In the short run, the market is a voting machine, but in the long run, it’s a weighing machine.” SIPs let you ride out short-term noise for long-term gains.

- Nithin Kamath, Zerodha’s founder, emphasizes: “The biggest mistake is not starting. Small investments today can lead to big outcomes tomorrow.”

These nuggets of wisdom underline why SIPs are a cornerstone of smart investing.

A Rs 10,000 SIP Success Story

Meet Priya, a 30-year-old IT professional from Bangalore. She started a Rs 10,000 SIP in an equity mutual fund in 2013, earning an average of 13% annually. By 2023, her investment grew to Rs 23.5 lakh—all while juggling rent, EMIs, and weekend getaways. “I didn’t miss the money each month,” she says, “but now I’ve got a down payment for my dream home.”

Priya’s story isn’t Rs 7 crore, but it’s real—and repeatable.

FAQs: Your SIP Questions Answered

1. What’s the Minimum Amount to Start a SIP?

Most funds let you start with Rs 500. Rs 10,000 is a solid amount for meaningful growth.

2. Are SIP Returns Guaranteed?

No, returns depend on market performance. Equity funds fluctuate but average 12-15% over decades.

3. Can I Stop or Pause My SIP?

Yes, most funds allow you to pause or stop anytime—no penalties.

4. How Long Should I Invest in a SIP?

The longer, the better. Aim for at least 10-15 years to maximize compounding.

5. Why Can’t I Reach Rs 7 Crore in 10 Years with Rs 10,000?

It requires an unrealistic 80% annual return. With 12-15%, you’ll hit Rs 22-27 lakh—still impressive!

Conclusion: Unleash the Power of Your Rs 10,000 SIP

A Rs 10,000 monthly SIP won’t make you Rs 7 crore in 10 years—not unless you’ve got a magic wand or a 80% return fairy godmother. But don’t let that discourage you. With a realistic 12% return, you can grow Rs 12 lakh of investments into Rs 22.18 lakh in a decade—or Rs 2.94 crore in 30 years. That’s the beauty of SIPs: small, steady investments, powered by time and compounding, can transform your financial future.

Ready to start? Pick a fund, set up your SIP, and watch your wealth grow. As John C. Bogle, Vanguard’s founder, said: “Time is your friend; impulse is your enemy.” Take the first step today—your future self will thank you.